Written by Jonny Fry

Written by Jonny FryWriters linkdin: https://www.linkedin.com/in/jonnyfry/

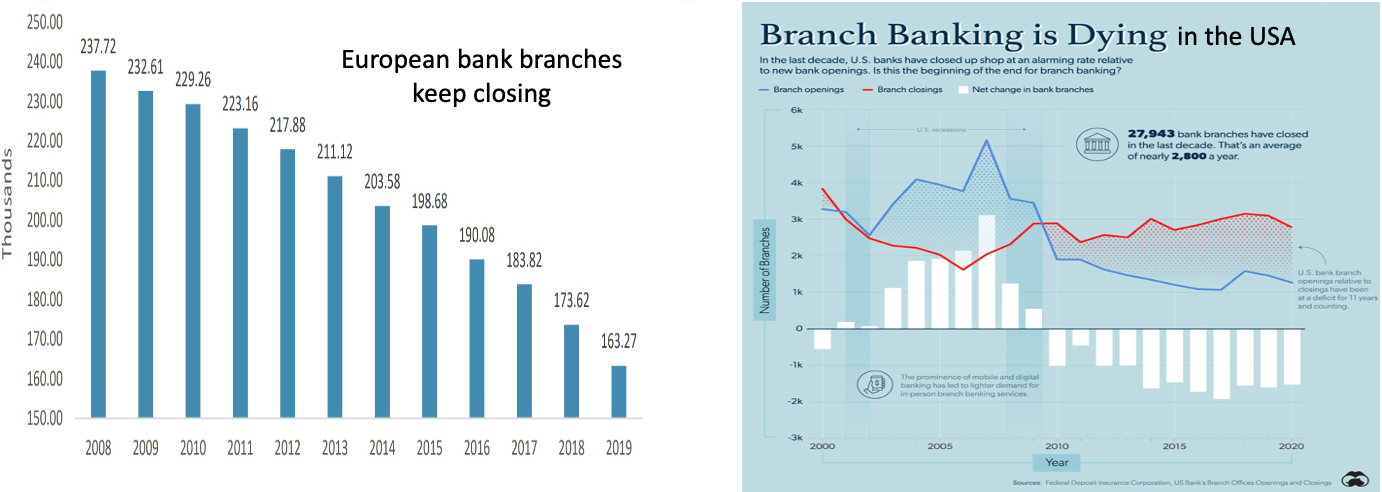

It could be argued that, since 2008, banks have had a torrid time globally as they desperately tried to repair their balance sheets and rebuild their capital reserves. The cosy cartel that many banks enjoyed has been challenged as they faced real competition from FinTech firms, with governments in various jurisdictions actively encouraging ‘challenger banks’ and ‘neobanks’ (on-line digital banking).

The payments eco system

Source: Insider Inteligence

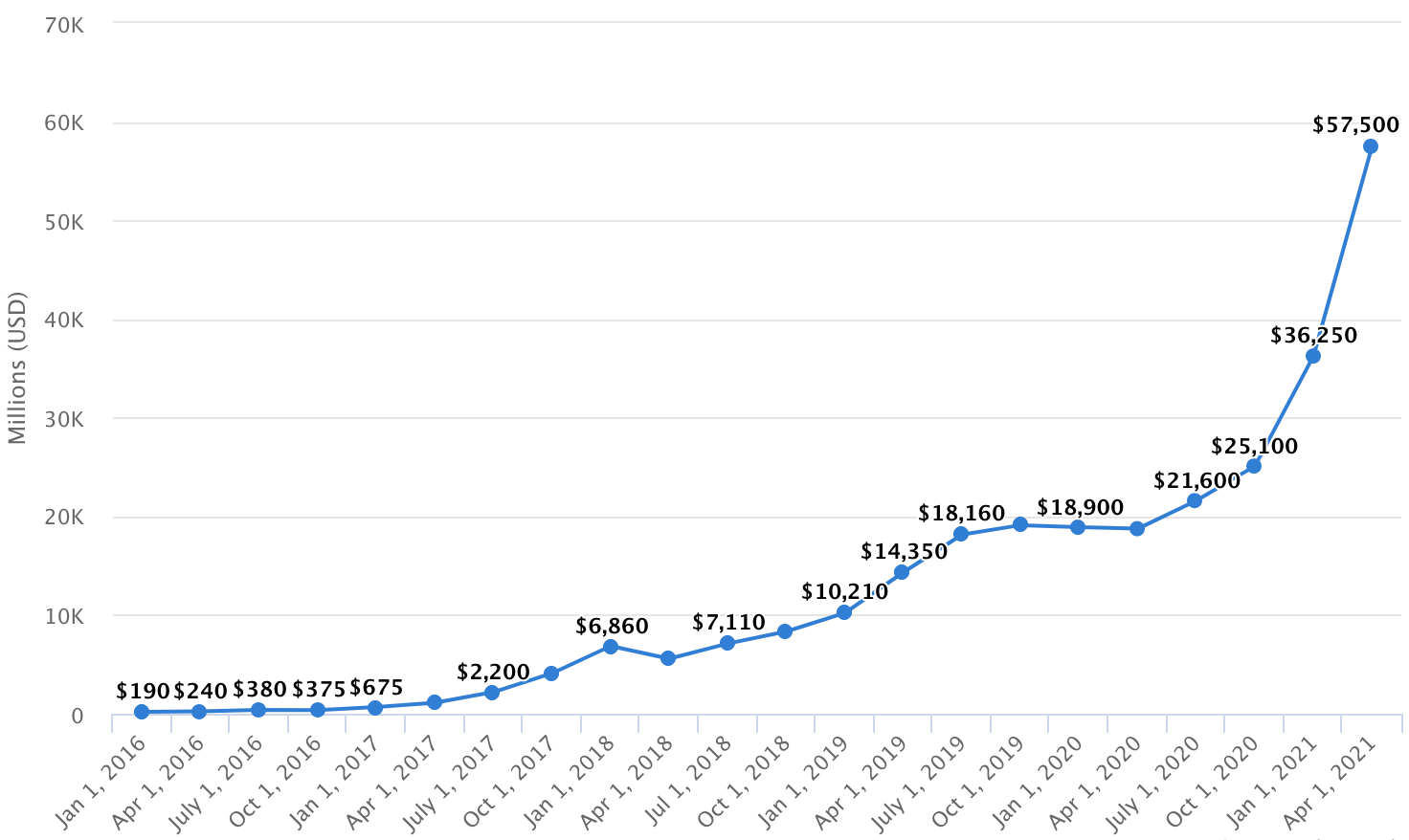

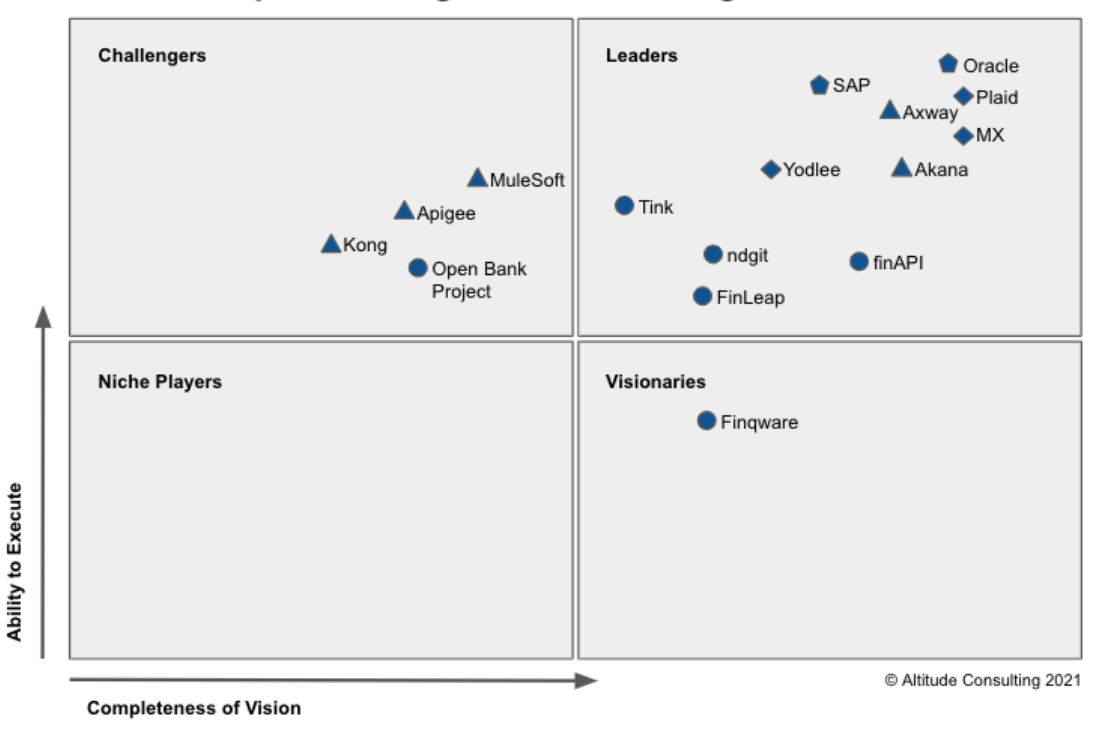

Whilst you will no doubt recognise some of the organisations above, many are unlikely to be familiar. With increasing competition from a variety of companies, this is the conundrum that many banks face. Some argue that with the growing interest in Decentralised Finance (DeFi) another wave of change and competitors are on the horizon. Biznewspost claims: “The coronavirus pandemic accelerated payments industry digitization by two to three years, as lockdowns, restrictions, and ongoing consumer health concerns upended daily life in ways that trickled into spending trends and consumer habits.” Habits such as, ‘Buy Now Pay later’, have offered stiff competition for traditional banks as companies including Klarna (Europe’s biggest Unicorn valued at over $1billion ), Affirm, Afterpay, and even Paypal (having just paid $2.7billion for Paidy, a Brazilian buy-now-pay-later firm), are making it easier for shoppers to obtain credit as they spread the cost of buying over a few months.. According to CB Insights: “E-commerce software companies that support online retail have seen surging investment in 2021, with $12.4B raised in the first half of the year — a 51% jump from all of 2020”.

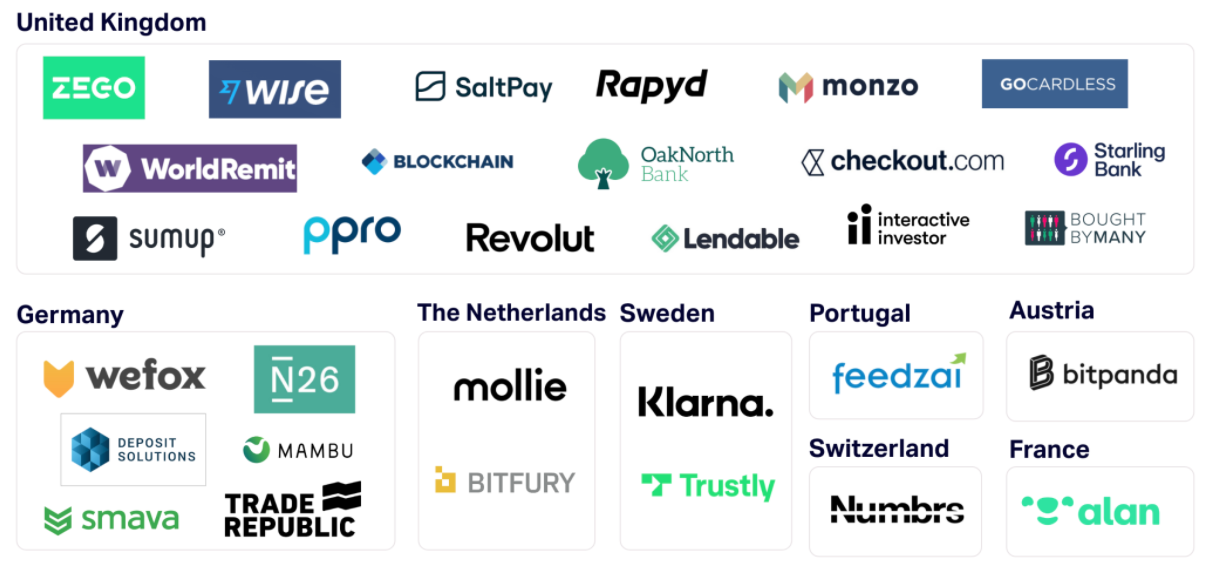

European FinTech Unicorns - firms worth $1billion+

Source: Sifted

According to CB Insights, there has been a tremendous growth in FinTech firms, with Europe now accounting for 25% of all 120 FinTech unicorns globally. A number of these FinTechs, and certainly many of the Payment platforms such as Google Pay, ApplePay (with 383million users), PayPal, Visa and Mastercard, are all accepting Digital Assets as payment.

Payment platforms are preparing themselves for the inevitable issuance of digital currencies from Europe, the US, the UK and Japan, to name just a few, with one of the most established payment cards, Mastercard, having recently acquired a US-based business crypto intelligence firm, CyberTrace. Meanwhile on the whole, banks have largely fought shy of Digital Assets. Indeed, it still is the case that, apart from Clear Bank in the UK, it is extremely difficult for those organisations engaged in cryptocurrencies to even obtain a bank account. This is also true in much of Europe. In Australia however, as reported by TechWire Asia: “Approximately 17% of Australians own a cumulative AU$7 billion worth of cryptocurrency.” Volt, a neobank, has teamed up with a crypto exchange to enable clients to trade cryptos and, more importantly, hold/store them in their Volt account. This potentially means that Volt will be the first bank globally to be able to offer clients the ability to store Digital Assets and be protected by a nation’s bank deposit insurance compensation scheme.

For a while the traditional banks have suffered from low Price Earnings with JP Morgan’s 2021 estimated PE 11.7; Europe’s largest bank, BNP Paribas, PE 8.8; Japan’s largest bank, MUFG, PE 6. If you compare this with some of the payment platforms’ PE - Visa 54.78, Mastercard 48.8 or Paypal 70 - you can see (in terms of which forms have the best prospects for future earnings growth) what investors are believing, as they are clearly rating the...

Source: Insider Inteligence

Whilst you will no doubt recognise some of the organisations above, many are unlikely to be familiar. With increasing competition from a variety of companies, this is the conundrum that many banks face. Some argue that with the growing interest in Decentralised Finance (DeFi) another wave of change and competitors are on the horizon. Biznewspost claims: “The coronavirus pandemic accelerated payments industry digitization by two to three years, as lockdowns, restrictions, and ongoing consumer health concerns upended daily life in ways that trickled into spending trends and consumer habits.” Habits such as, ‘Buy Now Pay later’, have offered stiff competition for traditional banks as companies including Klarna (Europe’s biggest Unicorn valued at over $1billion ), Affirm, Afterpay, and even Paypal (having just paid $2.7billion for Paidy, a Brazilian buy-now-pay-later firm), are making it easier for shoppers to obtain credit as they spread the cost of buying over a few months.. According to CB Insights: “E-commerce software companies that support online retail have seen surging investment in 2021, with $12.4B raised in the first half of the year — a 51% jump from all of 2020”.

European FinTech Unicorns - firms worth $1billion+

Source: Sifted

According to CB Insights, there has been a tremendous growth in FinTech firms, with Europe now accounting for 25% of all 120 FinTech unicorns globally. A number of these FinTechs, and certainly many of the Payment platforms such as Google Pay, ApplePay (with 383million users), PayPal, Visa and Mastercard, are all accepting Digital Assets as payment.

Payment platforms are preparing themselves for the inevitable issuance of digital currencies from Europe, the US, the UK and Japan, to name just a few, with one of the most established payment cards, Mastercard, having recently acquired a US-based business crypto intelligence firm, CyberTrace. Meanwhile on the whole, banks have largely fought shy of Digital Assets. Indeed, it still is the case that, apart from Clear Bank in the UK, it is extremely difficult for those organisations engaged in cryptocurrencies to even obtain a bank account. This is also true in much of Europe. In Australia however, as reported by TechWire Asia: “Approximately 17% of Australians own a cumulative AU$7 billion worth of cryptocurrency.” Volt, a neobank, has teamed up with a crypto exchange to enable clients to trade cryptos and, more importantly, hold/store them in their Volt account. This potentially means that Volt will be the first bank globally to be able to offer clients the ability to store Digital Assets and be protected by a nation’s bank deposit insurance compensation scheme.

For a while the traditional banks have suffered from low Price Earnings with JP Morgan’s 2021 estimated PE 11.7; Europe’s largest bank, BNP Paribas, PE 8.8; Japan’s largest bank, MUFG, PE 6. If you compare this with some of the payment platforms’ PE - Visa 54.78, Mastercard 48.8 or Paypal 70 - you can see (in terms of which forms have the best prospects for future earnings growth) what investors are believing, as they are clearly rating the...

#FrontierInsights

{kind=link}