Undoubtedly, there is growing interest in crypto currencies. In the UK, an FCA survey found that there has been a 20% increase in the number of people who now hold crypto assets. In its press release, the FCA reported: “Enthusiasm for cryptoassets is growing with over half of crypto users saying they have had a positive experience so far and are likely to buy more (rising from 41% to 53%). Fewer people also regret having bought cryptocurrencies, down from 15% to 11%”. It is not only in the UK. In a recent survey by SelfWealth, which is listed on the ASX and is one of Australia’s biggest on-line brokers with over 95,000 investors, it was found that “30% invest in crypto”.

According to CryptoFund Research, there are over 830 different funds investing in various forms of crypto assets. A PwC report looking at crypto funds established that “assets undermanagement had grown in 2021 to over $3.8 billion and the most common location for crypto hedge fund managers is the United States (43%), followed by the United Kingdom (19%) and Hong Kong (11%)”. Whilst the assets that many crypto funds invest in to are unregulated asset managers that are based in the UK that wish to manage crypto funds need to be regulated or be an appointed representative of a FCA regulated firm. As with traditional funds, there are key service providers that a crypto fund needs to have which, unfortunately, add to the total expense ratio (the true annual management fee) when running a crypto fund.

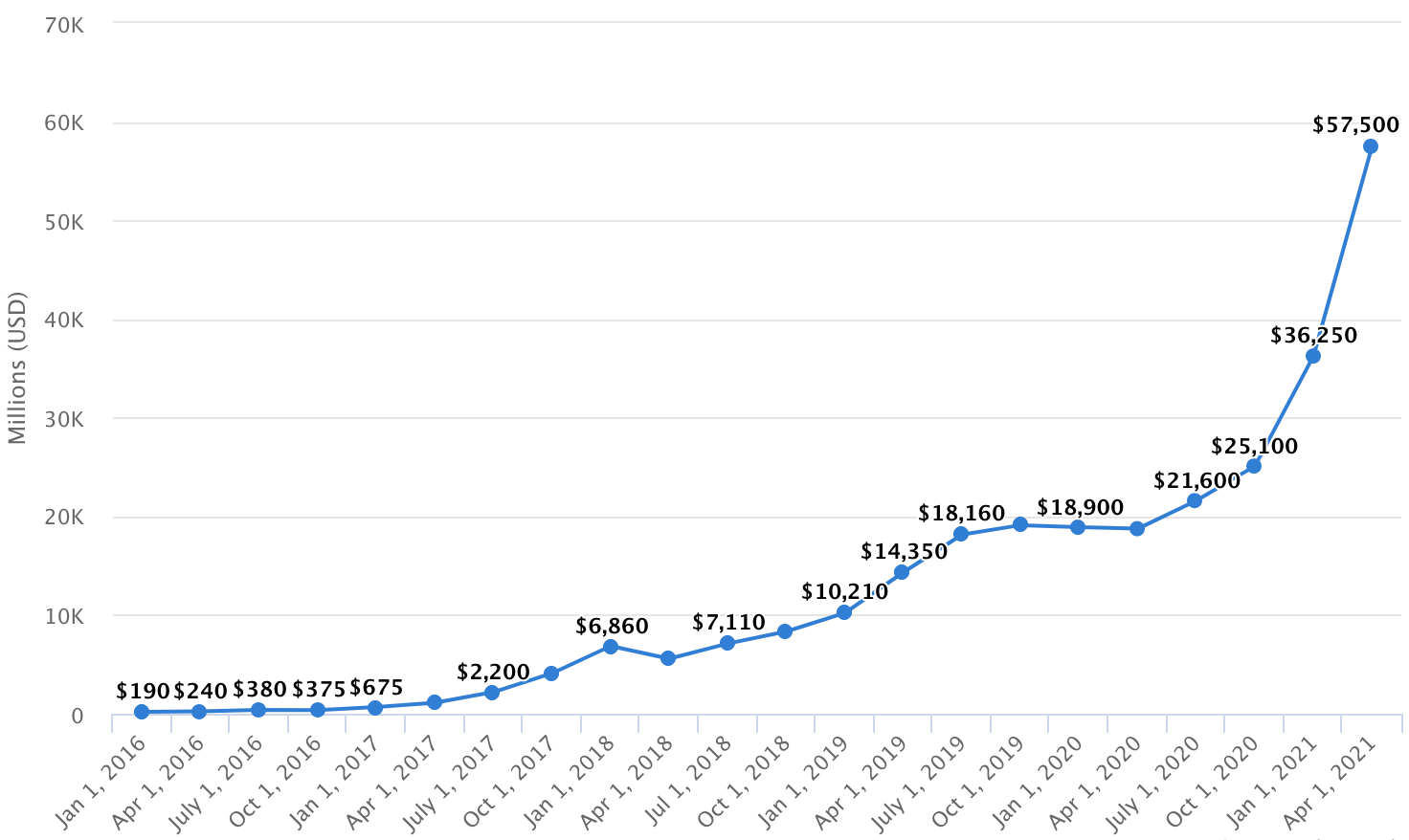

Growth of crypto funds

Source: Crypto Fund Research

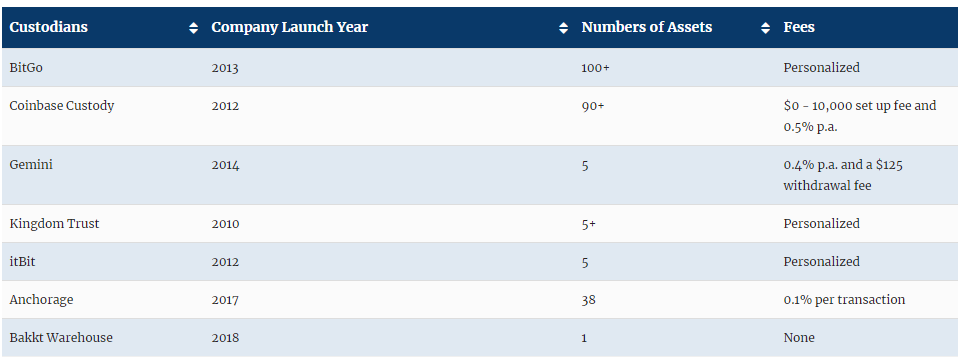

A crypto fund will need a custodian who is, in effect, responsible for ensuring that the assets in the fund are kept secure. Institutional investors pay close attention to the calibre of the custodian and look to them to ensure the capital they invest is safely held, and subject to strict procedures as to who is able to get access to the money in the fund. A selection of some organisations which offer crypto custody include:

Selection of crypto custodians

Source: Bitcoin Market Journal

The role of a custodian may now potentially be challenged due to the fact that Blockchain technology has brought about the development of Multi-Party Computation (MPC) which, itself, enables assets to be stored in multiple locations by a variety parties. This means that those custody firms which use MPC never have complete control of the assets and therefore do not need to be regulated and subject to the costs of insurance etc. As well as a custodian, crypto funds will usually use third party fund administrators who are responsible for calculating a fund’s value and will prepare investment reports for investors to monitor the activity of the fund in terms of performance and the assets that have been traded. Furthermore, the fund administrator is the one who prepares the fund’s financial statements. Here is a selection of crypto fund administrators:

As regards funds, there are two types for which asset managers can offer their services. A fund can be ‘open ended’ i.e., the size of the fund will increase or decrease depending on the number of investors who wish to buy or sell a fund. With this type, the fund manager calculates the net asset value (NAV) of the fund and then divides this by the number of units/shares/tokens in the fund. If someone wishes to buy into the fund, then more units will be issued at the price of the units based on the most up-to-date NAV. Alternatively, a fund may be ‘closed’. In this case, the fund manager initially raises a sum of capital and the monies are invested. If there are new investors who wish to gain exposure to the fund, then the fund price can trade at a premium to its NAV. If there are more sellers than buyers, then the fund’s price will trade at a discount to the NAV of the fund. The advantage of a closed ended fund is that the asset manager is not forced by investors to be required to liquidate/sell some of the holdings to meet redemptions. The disadvantage is that if the fund performs really well the asset manager is unable to easily expand the amount of money that he/she manages.

To date, because the underlying assets (that in a crypto fund) are not listed on a recognised exchange, the crypto funds themselves tend to have a high minimum initial investment - typically $100,000 - and are targeted at institutions, family offices and high net worth individuals, as opposed to the general public. As we see more ‘digital wrappers’ of existing equities such as Apple, Amazon and Tesla on Bitterx’s digital asset exchange, which trades 24/7, we could then see funds being made available for retail investors.