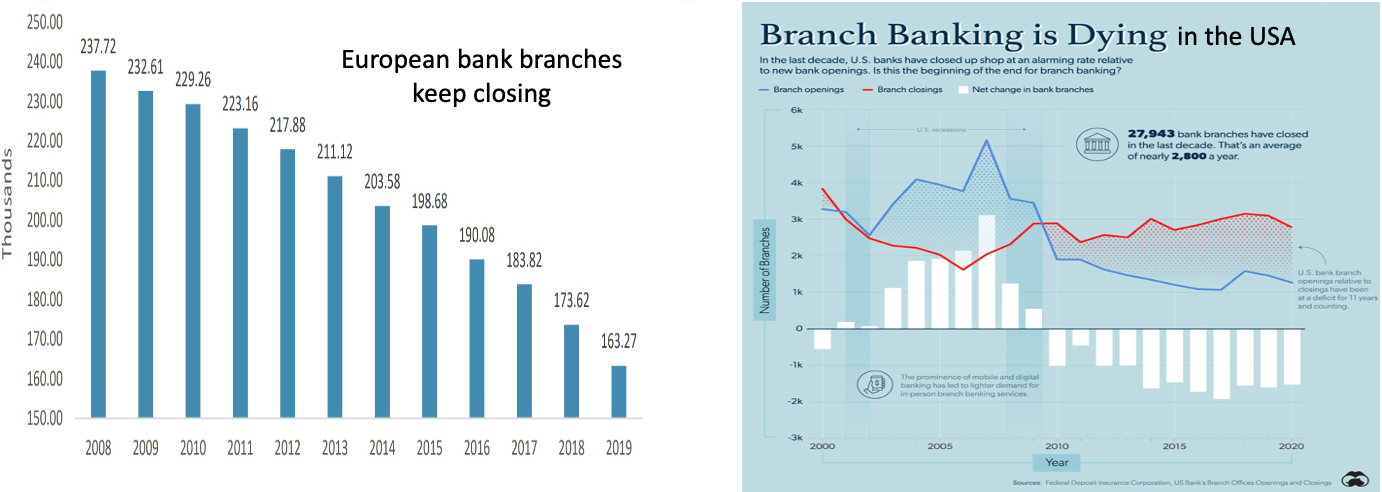

Arguably, the first signs of automation in the banking sector were the introduction of what we call in the UK ‘cash point machines’ or, as the Americans say, automatic teller machines (ATMs). The first ATM to be installed in the UK was in 1967 and a couple of years later, in 1969, an ATM was opened at the Rockefeller Centre in New York City. So, it is rather ironic that, while cash dispensing ushered-in banking automation, we are now witnessing the decline in the use of cash and the rise of digital currencies and the closure of bank branches.

Source: Payments cards and mobile.com Source: Visual Capitalist.com

However, the pace of change in banking had arguably been given a major boost due to the impact of open banking initiatives which, again, began first in the UK in 2018 and is now being adopted worldwide. The Open Banking Organisation defines open banking as “a secure way to give providers access to your financial information. It opens the way to new products and services that could help customers and small to medium-sized businesses get a better deal. It could also give you a more detailed understanding of your accounts, and help you find new ways to make the most of your money”. So, potentially open banking could be seen to be emerging as a huge disruptor for banks since it offers customers access to a greater choice of financial products and services; this also helps to explain the rise of so many fintech firms.

Accenture has recently highlighted in a report on open banking that:

-

“ the global open banking waters are relatively calm right now, but beyond the horizon a wave of change is building.

-

banks will soon need to choose between catching this wave or riding it out and hoping for minimal damage - up to $416 billion in revenue is at stake.

-

open banking will arrive at different times in different markets but when it takes off, growth will likely be rapid - sceptics may be left behind.

-

tomorrow’s open banking leaders will prioritise data custodianship, analytics mastery, agile partnerships, and trusted security.”

There exists a very wide selection of open banking platforms and some have become extremely successful. For example, Klarna is thought to be Europe’s most valuable start up and worth over €31billion. It is interesting to see recently that it was the payments platform, Visa, not a bank, which acquired the Swedish firm, Tink, for €1.8 billion. Visa had been disallowed by the Justice Department to acquire US-based Plaid in January 2021 for $5.3 billion . At the time it was thought that Plaid would pursue a public listing. Plaid is now estimated to be valued at $13+billion, therefore will we see a bank attempt to acquire Plaid before it lists or will a bank make a bid before it is purchased by another fintech?

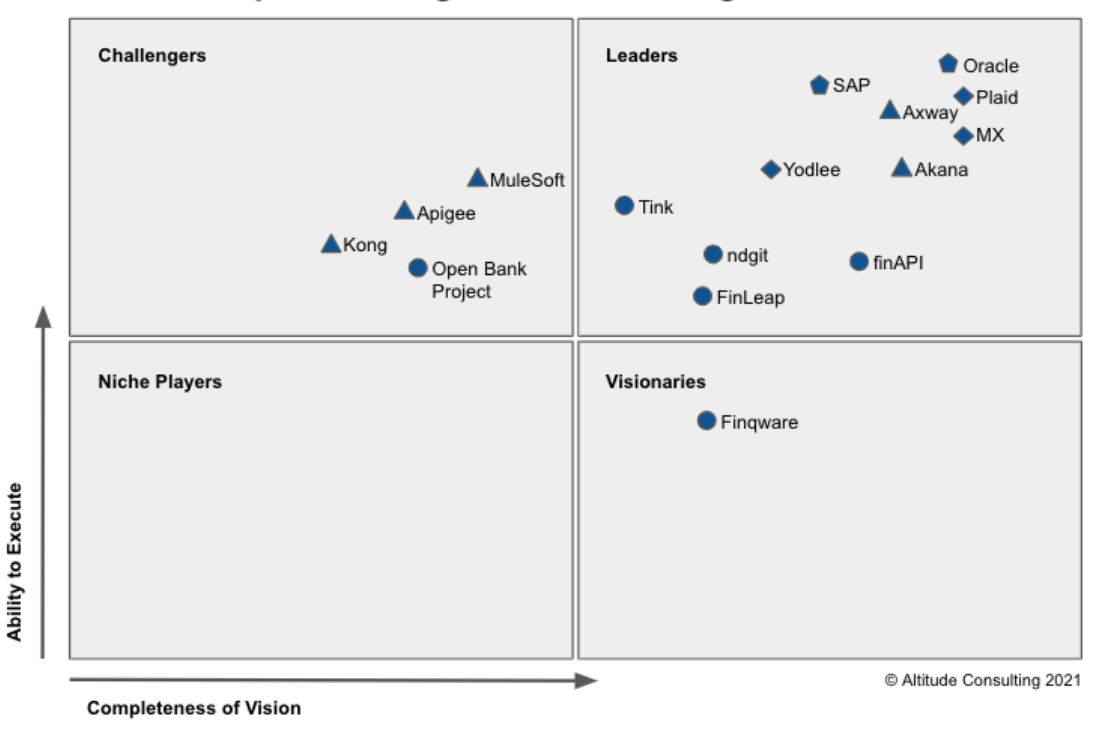

Achieve open banking platform rankings 2021

Source: Achieve Consulting.com

Furthermore, as the publication the Entreprenuer has highlighted, banks face a number of challenges including:

-

legacy systems - designed over a decade ago and unable to adapt to today’s connected digital environment

-

deep silos - banks have long been siloed organisations, driven by design and regulations

-

customer evolution - fast-changing behaviour of today’s socially connected, digital, next-gen consumer

-

compliance demands - growing compliance and costs spurred by many post-recession regulatory mandates.

Interestingly, Blockchain technology offers open banking platforms and banks some potential solutions and a foundation for a new digital financial system. Blockchain-powered platforms allow a new digital financial ecosystem by layering distributed ledger technology on top of what were originally analogue, paper-based legacy banking APIs, whereby enabling third parties to interact securely with banks and their data without directly accessing the core banking systems. Financial institutions can use such platforms to transact securely with each other (in what is, after all, a trust-less environment), sharing information and connecting different parties so as to create more robust and decentralised networks on a shared platform in a much more collaborative manner. Since Blockchain technology relies on securing information in a cryptographic basis and can hold information on a decentralised basis, it can reduce the chance of hacking whilst equally improving financial institutions’ disaster recovery plans and infrastructure. It is possible for customers’ data to be categorised, such as highly classified and private customer data, bank sensitive data, third party use data and general public data - all managed in various blockchains. Access and disclosure for each category can be programmed using smart contracts, thus enhancing data protection and minimising security risks, and allowing the customers much greater control over their information. Smart contracts can empower customers so that they, themselves, decide who has access to what data, when, and for how long.

The blockchain-powered platforms used enable aggregation and storage of data that can be relied upon to develop new products and services such as loans, investment packages and pension plans, etc - bespoke for a customer’s financial status. Hence, Blockchain technology lends itself to be very appealing for open banking as it only allows access to pre-approved data in a secure, auditable and non-intrusive manner. Understandably, this improves trust and enables banks to only share the requisite information without compromising user privacy and data security. Furthermore, by hashing data (i.e., by encoding the information) it prevents unauthorised users from reading data that is stored in this unreadable format.

Undoubtedly, we are beginning to see more and more organisations using Blockchain technology. In the US, Compass Bank is using Tassat’s platform to enhance its Business2Busines (B2B) payments services. Tassat tokenises U.S. dollar deposits at banks whereby providing secure, faster and cheaper instant payments and thus avoiding overnight settlement and processing delays since it offers settlement in real-time. Meanwhile in Japan, Sumitomo Mitsui Banking Corporation is using Contour’s banking and corporate network which aims to digitise the letter of credit settlement processes using R3’s blockchain platform, Corda.

{kind=link}