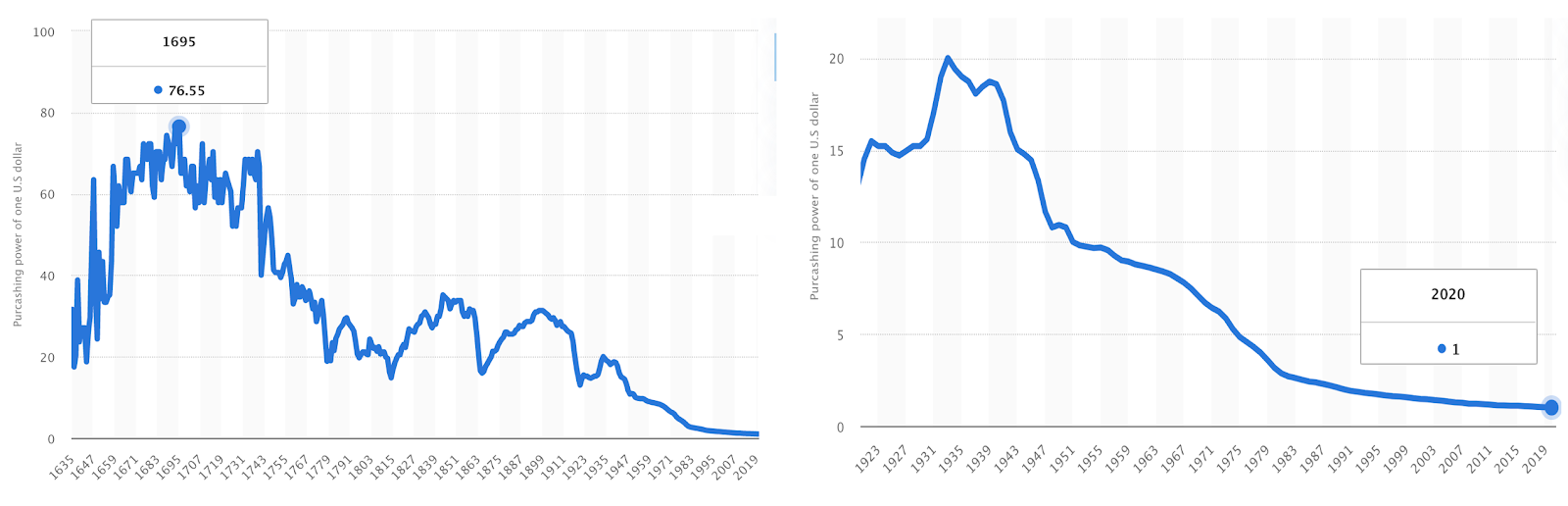

The term stablecoin, a digital currency backed by US$s, could be seen as somewhat misleading for American citizens since they will have witnessed the value of their $ fall in value over time. The lack of stability/buying power can be seen due to the impact of inflation. One US$ in 1695 would be worth 76.5 times than it is today or, to think of it another way, one US$ in 1935 is worth 20 times what it can purchase today.

Source: Staitisa.com

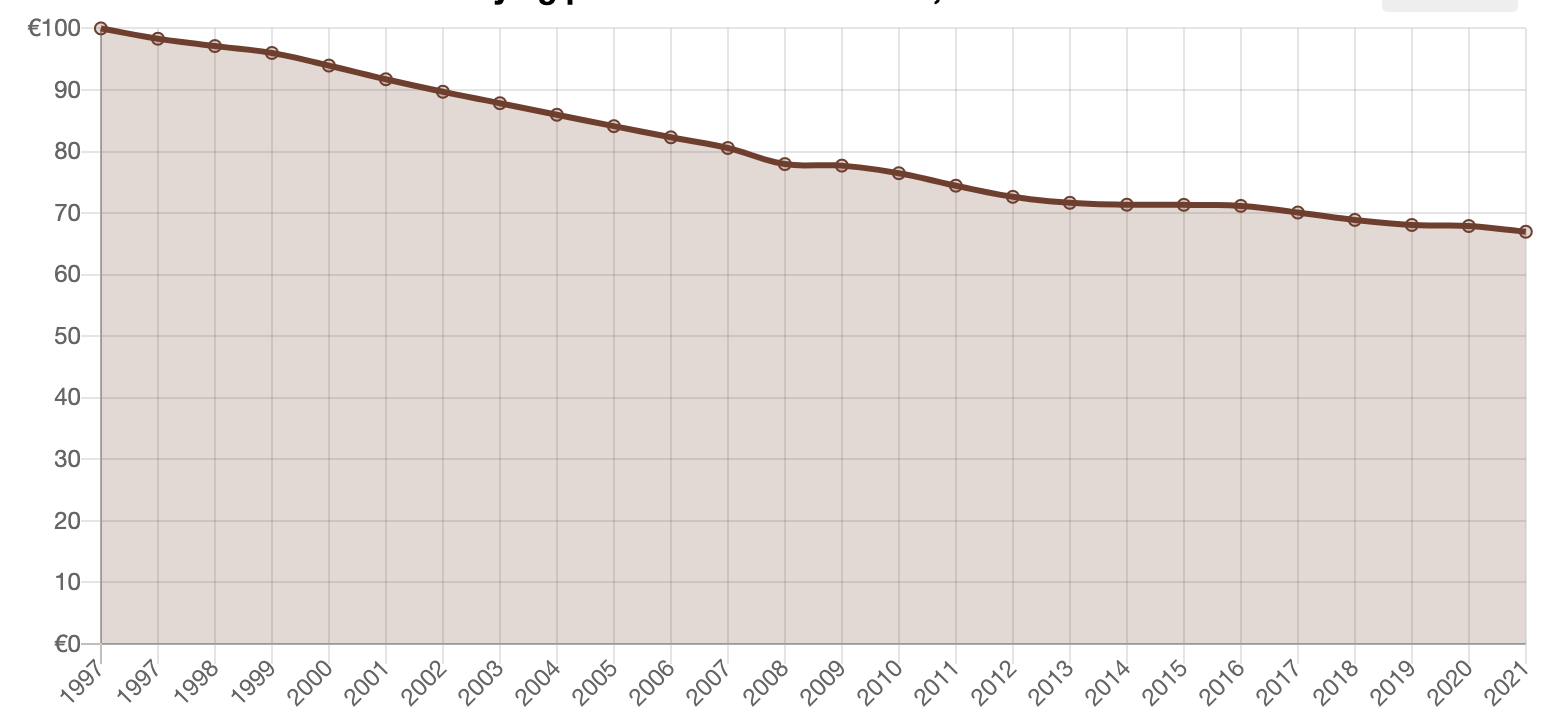

The impact of inflation is not confined to the $. Since its launch, the Euro has fallen in value by almost 33%. Hence the need to ensure that you have your investments in the long term, protected from the ravages of inflation in real assets. Yet despite this, many of us keep money in a bank?

Fall in the purchasing power of the Euro

Source: in2013dollars.com

Notwithstanding the impact of inflation, would it not be more accurate to refer to a fiat-backed digital currency as a pegged coin (as opposed to a stablecoin) since surely stability is a relative and not an absolute description? Digital currencies, backed by a fiat currency, arguably fall into two categories - Central Bank Digital Currencies (CBDC) or stablecoins (typically issued by non-government organisations). Regardless of what you call a digital currency, backed by $, £, €, CHF or Yen etc, there are a number of advantages and disadvantages surely worthy of consideration for digital currencies. Stablecoins were once dismissed as a way to store ‘ill-gotten gains’ when ‘crypto whales’ wanted to reduce their exposure to crypto currencies, and neither could access $ in a bank account nor wanted to deal with a traditional financial institution. Ironically, going forward we could see regulators being supportive of digital currencies and possibly insisting that issuers of income producing assets (such as equites and bonds) change the frequency of income payments. A stablecoin would enable customers to be treated ‘more fairly’ since stablecoins could facilitate digital equities and digital bonds to make income payments more frequently, e.g., weekly. The income due to an investor could be calculated based on the number of days a security has been held, as opposed to waiting for monthly coupons from bonds or six-monthly dividend payments.

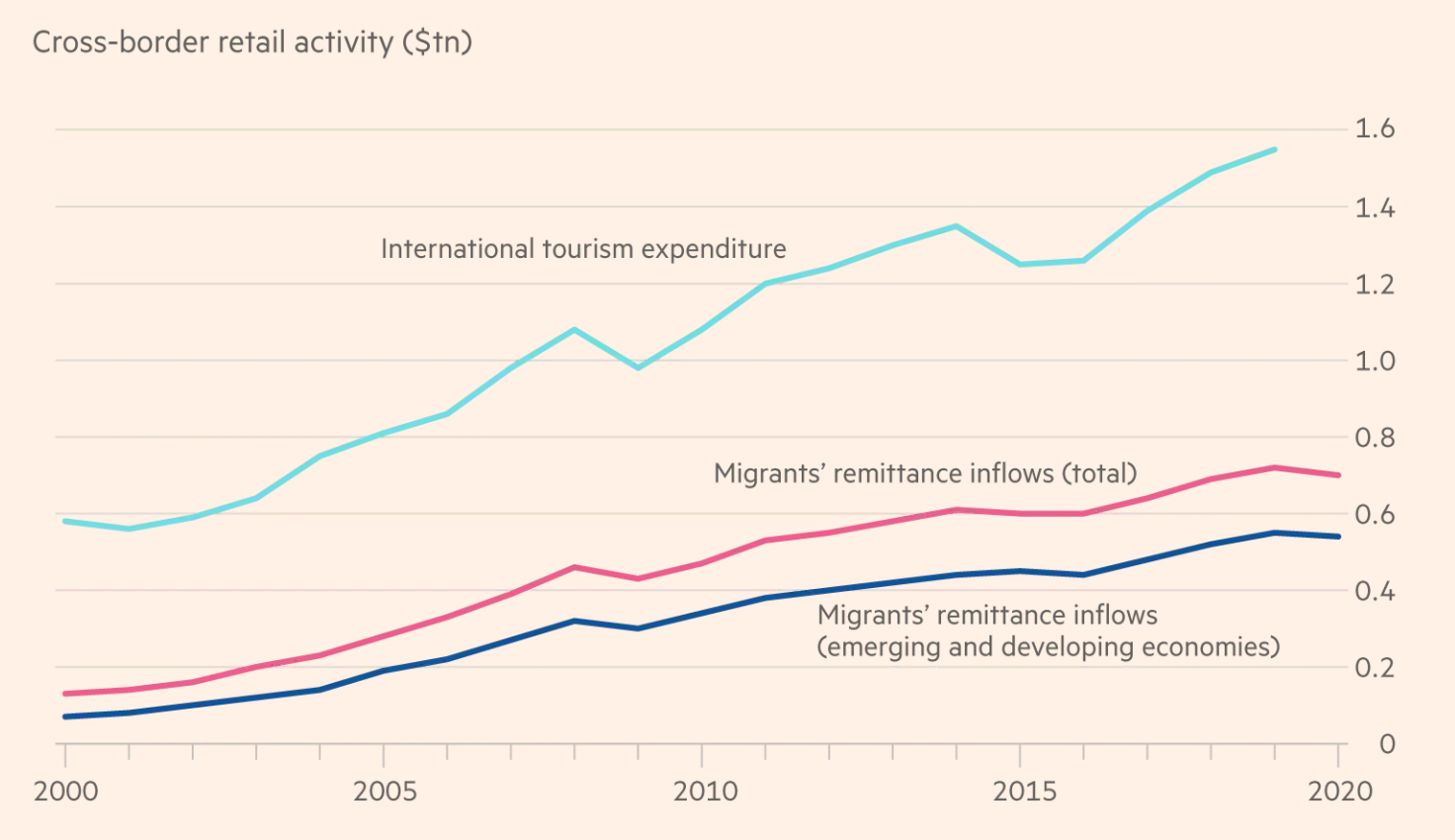

Another advantage of a digital currency is that it reduces the costs and time taken to remit money, as well as reducing the cost of money spent by tourists when overseas. This is likely to impact many of our readers who travel overseas or indeed run their own businesses, especially if they are trading with overseas suppliers and/or customers.

Size of retail cross boarder payments

Source: Bank of International Settlements

Challenges to be addressed:

-

infrastructure - this is the technology behind digital currencies which is able to handle the volume of transactions

-

potential environmental impact of some Blockchain technologies

-

privacy of users

-

interoperability - how will digital currencies be able to interact with cash?

-

decentralised vs centralised technology - in a truly decentralised environment, if there is a problem, who is held to account: ‘Mr and Mrs Bitcoin’?

-

those who prefer, or are only able to use cash - according the Bank of England, “Today, there are currently 1.2 million unbanked people in the UK, who by and large rely on cash and cannot access digital payments or can access them only at disproportionate cost”

-

loss making - given current interest rates, stablecoins cost, not make, money.

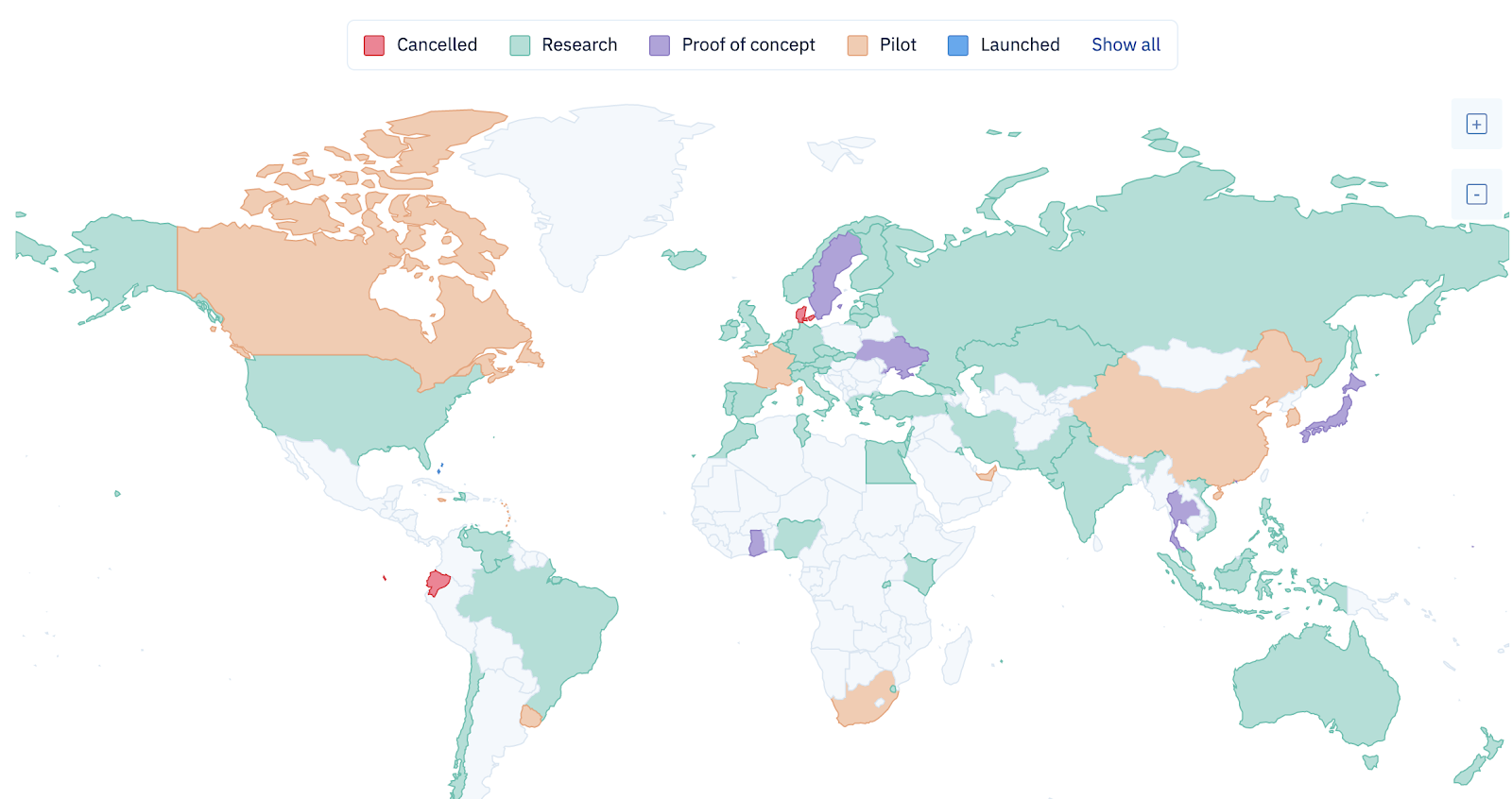

Central Bank Digital Currency status

Source: CDBC Tracker

For an update on what different countries and their central banks are doing, please click here for a website which is regularly amended and which details the progress of various CBDCs.

Possible use cases for stablecoins:

-

payment of income - dividends, coupons, rent, income on structured products

-

corporates - purely in-house to improve efficiency for corporate treasury departments

-

collection and payment of insurance claims and premiums

-

debt instruments - HSBC claims it is up to 90% cheaper to issue digital bonds using Blockchain technology; as more bonds are issued this way, how long before coupons are paid digitally? - €100m EIB bond, the World Bank Bondi Bond (two issues totalling AU$160m)

-

digital equities - Bitterex is offering exposure to Apple, Tesla; the Swiss are enabling the issue of digital equities, as opposed to paper-issued stocks (and thus the need for digital payments)

-

new asset classes creating the need for digital settlement - DeFi, crypto, NFTs

-

microfinance - a market expected to reach $313 billion by 2025, much of which will be via mobile devices

-

online market - $4.3 trillion, growing at 11.8% in the US

-

1.7 billion unbanked - the World Economic Forum believes digital currencies can help the global unbanked; many of the 1.7 billion have no bank account but they do have a mobile phone

-

Euro stablecoin - with monthly attestations by PwC for the French supermarket, Casino, as part of its customer loyalty plans

-

Visa clients have spent $1billion of crypto in the first half of 2021

-

Mastercard is to offer crypto payments using USDC

-

in April 2019, Société Générale (via its subsidiary, FORGE) issued a digital bond of €100 million on a blockchain. Maybe we can get its London office to start issuing Sterling-based debt instruments, and the coupons’ income could be payable using a Sterling stablecoin

-

Société Générale has also issued a digital structured product internally using a blockchain, and it intends to begin selling such products externally to wealth managers/IFAs in 2022. Many structured products are designed to pay an income so, again, there could be a need for a sterling version. As an aside, Bloomberg claims the total structured product market accounted for over $7 trillion in invested assets.

-

HSBC claims it is 10 times more efficient to issue digital debt using blockchains, so why would it not then pay coupons digitally, via a stablecoin?

-

DeFi sector offers access to EURt (Tether Euro stablecoin) for lending and borrowing but it can also be done by using Tether’s USDT. This is possible by using the DeFi app from Cream Finance.

It seems inevitable that it is not if, but when, we will see many other countries follow the lead of China, the Bahamas, Antigua and Barbuda and Saint Lucia, which have launched their own CBDCs. According to Mckinsey, middlemen and intermediaries involved in payments around the world made as much as $2trillion from their services in 2019 alone. Digital currencies are expected to be able to remove a large part of these transaction fees and, if successful, will be a benefit for us all. There is growing interest that, as more and more CBDCs are launched, these Digital Assets are seen as being able to bring greater efficiency and a reduction in costs to payments as well as offering governments a new tool with which to control their economies. Furthermore, the need for stablecoins will grow, too, as we see the rise of Digital Assets backed by real estate, equities and bonds - not to mention the new investment opportunities being created in the crypto, DeFi and NFT sectors.