It would seem, on the face of it, that many so-called sophisticated Western economies and their central bankers are juxtaposed to the way in which China is approaching digital currencies. The Chinese are continuing to roll out their own version of a Central Bank Digital Currency (CBDC) to cover a total of 10 cities, spanning 100 million people. According to Coinidol: “Over 200 vendors employed to hold the 2022 games began enabling digital payments conducted with the help of e-CNY. Among other items, the Chinese will be able to buy the Olympic tickets using the CBDC at least at some venues. Beijing and Shanghai are planning to distribute a total of more than 550k digital red envelopes each having about $31.5 USD of e-CNY to people around the two cities.” As Reuters reported back in April 2021, China has proposed new rules for CBDC, quoting:

-

“Interoperability should be enabled between CBDC systems of different jurisdictions and exchange;

-

Information flow and fund flows should be synchronised so as to facilitate regulators to monitor the transactions for compliance;

-

A scalable and overseen foreign exchange platform supported by DLT (distributed ledger technology like blockchain) or other technologies.”

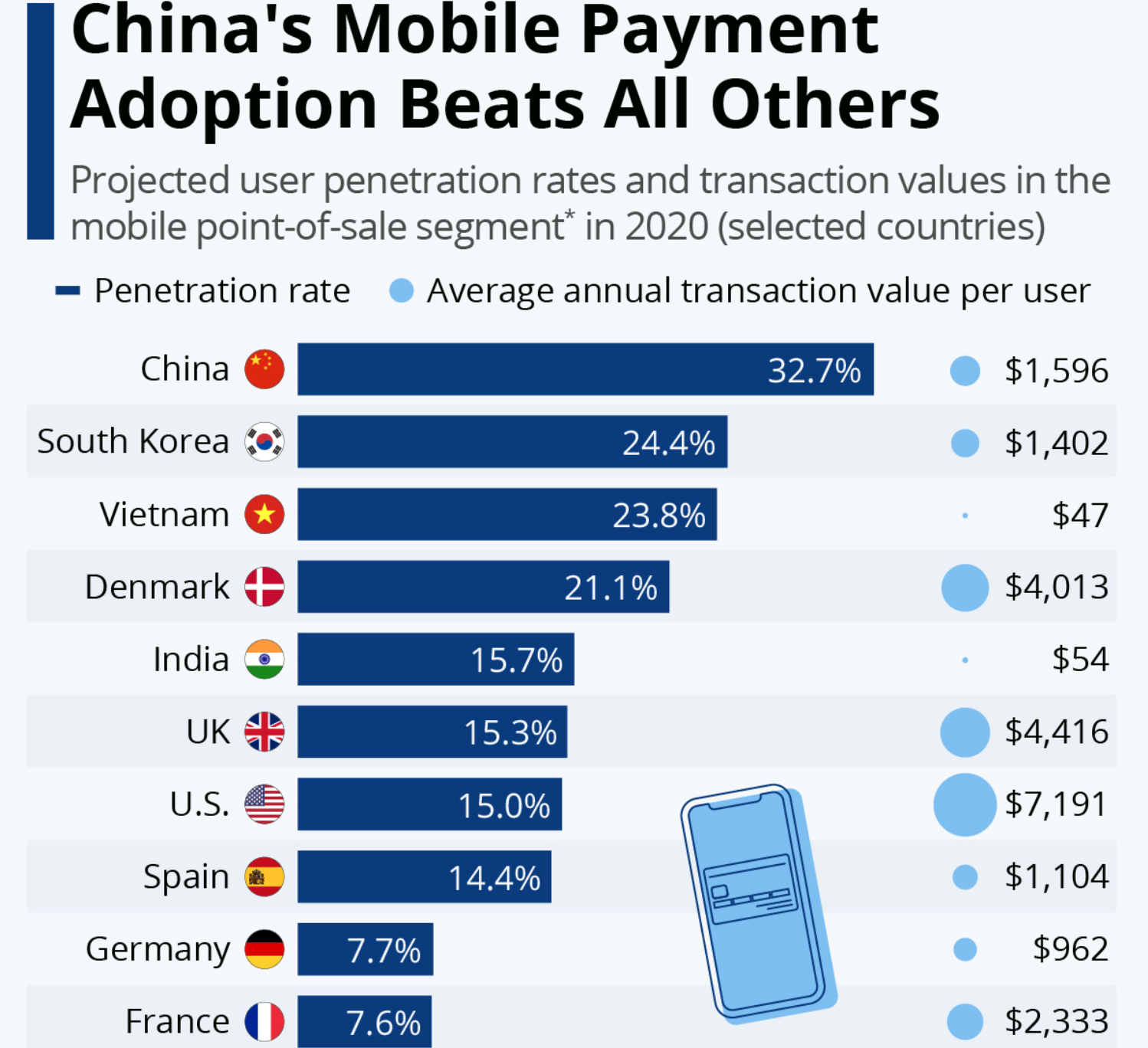

China’s use of mobile payments leads the world

Source: Statista.com

It may or may not be related, but the Chinese Banking and Insurance Regulatory Commission has introduced new regulations on the $1.15 trillion cash management products in China. Will the next overture for China be to ask for a % of these massive savings to be transferred to its new CBDC?

Meanwhile, the Guardian newspaper has reported: “The Basel Committee on Banking Supervision, which consists of regulators from the world’s leading financial centres, is proposing a “new conservative prudential treatment” for crypto-assets that would force banks to put aside enough capital to cover 100% of potential losses.”. Stablecoins, pegged to a country’s official currency, would not be subject to the same strict rules as they are deemed to be more akin to traditional assets such as bonds, loans, deposits, equities or commodities. As reported in the Herald of Scotland , Britain continues a relentless march for using less and less cash with the number of cash payments dropping by 35% in a year - only 20% of payments now involve notes or coins, as opposed to 50%+ ten years ago.

The Fed, the ECB and the Bank of England have all declared that they are investigating the potential of CBDC, but one cannot help wondering what powerful lobbying is occurring behind the scenes by those banks desperate to maintain the status quo which has served them so well to date. Bizarrely, many Western governments and their regulators seem fixated that Digital Assets will continue to offer money launderers a panacea to enable them to make payments, whereby ‘oiling the wheels’ of illicit activities. This recent argument by a Dutch official, as reported in Cointelegraph, is such an example: “Ban Bitcoin because it doesn’t meet any of the three functions of money and is handy for criminals”. Such concerns are understandable given the rise in cyber attacks and ransom demands, often with the ultimatum for payment to be in cryptos e.g., the Colonial Pipeline which resulted in a payment of $4.4million Bitcoin. However, there could well be signs that demanding cryptos as a form of payment may not be such a panacea for criminals. In the US, the Fed has succeeded in retrieving $2.3 million of the Bitcoins paid by the owners of the Colonial Pipeline, thus sending a warning shot across the bows of the perpetrators of ransom that they may be better off reverting to demanding suitcases of cash, diamonds or gold as they have done in the past! Then again, the banks and those who regulate them know a thing or two about deficient Anti Money Laundering (AML) procedures and checks as, in the first quarter of 2021 alone, banks where fined over $1.25 billion for AML transgressions.

Unsurprisingly, the adoption of Digital Assets is growing with over 10 million people already owning this asset class - up 55% from last year. Subsequently, TheCityUK, a lobbying group for Britain's financial services sector, is hankering for the UK to introduce regulation for the cryptocurrency sector. TheCityUK believes the UK could influence global policy by establishing guidance for regulating cryptos and thus attract businesses to the UK by offering legal certainty. Miles Celic, chief executive of TheCityUK, recently said: "There is a fierce global race underway to see which applications of DLT [distributed ledger technology] and cryptoassets will win out, and who will grab the biggest slice of the value they promise. The ultimate winner is for markets to decide, but government and regulators have an important part to play. They must set safe and robust rules for this burgeoning sector – while ensuring they don’t inadvertently squash good ideas before they can mature and flourish."

So, whilst China pushes forward and extends its already sizable lead when it comes to making payments digitally, much of the rest of the world is struggling to set rules and regulations - pontificating instead, as opposed to acting more decisively.