Written by Jonny Fry

Written by Jonny FryWriters linkdin: https://www.linkedin.com/in/jonnyfry/

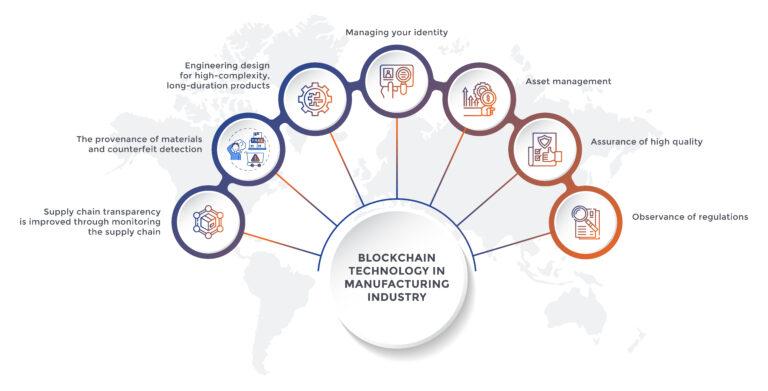

Blockchain has the potential to provide unprecedented levels of supply chain transparency to the manufacturing industry. Blockchain-powered platforms can improve transparency through the production process, from sourcing and procurement to the shipment of the final product as well as (in almost real time) monitoring and reporting of the servicing of machines on the factory floor. One of the most critical aspects of production is the supply chain. However, acquiring visibility into each supply chain component that spans numerous enterprises, states or nations can be challenging.

In addition, there is frequently no standard way of documenting, storing and transmitting information, especially when dealing with global supply chains that involve many jurisdictions. According to East Asia Forum.org: “A single cross-border trade transaction involves the exchange of an average of 36 different documents and 240 copies of such documents”. Distributed ledger technology, known as blockchain technology, has the potential to improve, modernise and fortify supply chains by providing transparent and secure product tracking at every stage. The audit trail is visible in real-time and documented as blocks in a chain, so there is no guesswork along the supply chain as to when goods are shipped, who has handled them or when they will arrive. Greg Cline, head of research for Aberdeen Group's manufacturing, product innovation and engineering practices section, explains: "Many manufacturers are enthusiastic about blockchain's potential capacity to authenticate items going through the manufacturing supply chain." So, given the highly transactional and frequently multi-step nature of business process services, the potential uses of blockchain technology in manufacturing are substantial.

Source: msrcosmos.com

What are the benefits that blockchains offer manufacturers?

Although blockchain technology may have been initially developed to streamline cryptocurrency transactions its underlying principles are adaptable to the manufacturers, such as:

-

reduction of administrative expenses and entrance obstacles - blockchain technology might significantly lower the threshold for new entrants by reducing the cost of maintaining a manufacturing business. The blockchain-enabled business model of "machines as a service" (MaaS) allows firms to save money by leasing rather than buying machinery. This new form of conducting business will make it easier for up-and-coming manufacturers to obtain their goods to market without the need to borrow large capital sums.

-

persistence and firmness - as a result of COVID-19, manufacturers have been obliged to review their supply chains and methods of production. Blockchain technology is able to help strengthen the resilience of a manufacturing company, even whilst there is no silver bullet for dealing with disasters such as a worldwide pandemic. The decentralised nature of blockchain technology ensures that blockchains can function even if a single node fails or a single participant leaves the network. When it comes to building a robust business strategy, the consistency provided by blockchain technology is invaluable to manufacturers.

-

trust and openness are strengthened - businesses that wish to earn the trust of various third parties such as suppliers, distributors, shareholders, staff, and potentially the end customer, are able to offer greater transparency using blockchain technology. Distributed ledgers store data in a single, immutable copy that all nodes can access in the network at all times.

-

improved security - blockchains store data using intricate cryptographic coding to ensure the security of the information that they hold. Blockchain's openness is matched with stringent safeguards in the form of cryptographic signatures on each transaction. Since the network's storage is also distributed, the ledger and the information it contains are safer against cyberattacks as not all the data is held in just one location.

How blockchain is used in manufacturing

-

verifying the origin of materials

Falsified products and fraud in the supply chain have been a problem for many manufacturers for years, whether it be horsemeat being used for human consumption or corrupt medical supply chains. Hence, manufacturers are looking to blockchain technology to build an immutable ledger of assets and products. With the use of blockchain technology, a distributed digital ledger can be created which solves issues with the distribution and dissemination of data in a decentralised supply chain. A safe, permissioned database is available to vendors, but no single organisation claims sole custody of the information contained inside. As a result, the possibility of fraudulent data alteration by some vendors is greatly reduced. In addition, the inaccuracies and delays that come with paper-based audit trails are eliminated with the use of blockchain technology in manufacturing. Those in the manufacturing business may now check the provenance of their materials and keep fake goods out of the supply chain. An immutable audit trail is achieved while the danger of fraud is decreased.

-

supply chain management

One of the most time-consuming and essential business activities for manufacturers is supply chain management. Using blockchain technology, factories can track more accurately the whereabouts of raw materials, components and finished goods. Blockchain's definitive end-to-end path for parts and products enhances track-and-traceability, whereby improving accuracy and reducing production mistakes. Japanese manufacturer, Toyota, is now able to tracks auto parts across multiple jurisdictions, factories and suppliers, sharing information on a real-time basis with manufacturers, banks, distributors, insurers, government authorities and customers by using blockchain technology - thus reducing recall rates and increase safety.

-

automated contractual terms (smart contracts)

The introduction of smart contracts made possible by blockchain technology has revolutionised the manufacturing industry. Smart contracts are computer codes that may be found on a blockchain, eliminating the need for paper contracts or fragile digital reproductions of paper contracts. The use of smart contract enable greater automation of many of the current paper-based systems which manufacturers have historically relied upon, so streamlining otherwise intricate corporate procedures. The terms and conditions and data stored on a blockchain may be utilised to offer more accurate inventory tracking, supply chain monitoring, payment timing and processing in a highly transparent manner to engender greater levels of trust in the manufacturer. By switching from manual to automated procedures, businesses may save time, energy and money.

-

quality assurance and regulatory compliance

As a result of its inherent security and capacity to monitor a single version of a piece of information, blockchain technology can be helpful for a manufacturing a company's quality control and regulatory compliance demands. Blockchain technology may reduce errors in the quality control process by using machine-level monitoring and exact track-and-trace of materials and components. As a result, there are fewer product recalls and less material goes to waste, both of which drive higher levels of profitability. A second advantage is that the blockchain ledger cannot be altered. This includes machine information, production methods, raw materials, and more. Internal and external auditors can utilise these records to verify safety precautions (all legal requirements) as well as helping to monitor companies’ ESG credentials.

A Capgemini study has found that nearly 15% of manufacturers are either implementing blockchain technology or have a pilot project. Of this group, over 60% say that the technology has already transformed the way they collaborate with others in the supply chain and that they plan to increase their blockchain investment by 30% in the next three years. In 2021, the current blockchain technology market size was only $5.7billion but is predicted to grow by 87% p.a. and be worth over $1.59trillion by 2030. It is highly likely then that we will see many more manufacturers adopting the technology going forward.