Written by Jonny Fry

Written by Jonny FryWriters linkdin: https://www.linkedin.com/in/jonnyfry/

Despite the recent falls in the value of cryptocurrencies - the market capitalisation of the crypto market has fallen from $3trillion to under a $1trillion - there is a growing number of institutions offering access to digital currencies. Incredible really….. when you consider how small the actual crypto market is, many financial newspapers and the press in general still mention it on a regular basis. By now many will be aware that the biggest crypto, Bitcoin, is still accounting for over 38% of the entire crypto market capitalisation.

Having risen in value from $0.01 to (at one stage) over $64,000, the fear of missing out (FOMO) would still appear to be a strong driver amongst private investors and institutions alike. Although cryptocurrencies are highly volatile and still a small asset class, almost every week another regulated financial services organisation launches a new service or announces its engagement with cryptos. And when you see former FBI staff making statements such as this one - “Unlike other forms of fraud in fiat, with cryptocurrency in the blockchain… there’s a record… and that transparency and speed of accessing that record globally makes investigations of these types of fraud accelerate over traditional finance” - from Gurvais Grigg, Chainalysis’s CTO and former FBI Assistant Director, it is easy to understand why we are seeing ongoing interest from banks, asset managers, exchanges, etc.

The adoption and growth in the infrastructure which enables cryptos to become even more mainstream shows no sign of abating. Mastercard has sponsored a survey of 35,000 people and found that 91% had heard of crypto and half were interested in using crypto to mail payments, and recently CNBC has reported: “Mastercard and Visa have both been signing up new partners and become even more involved in the crypto sector”. Mastercard has teamed up with crypto firm Bakkt to let banks and retailers offer crypto-related services. Visa, has more than 70 crypto partnerships and has now agreed a deal with FTX to offer crypto debit cards in 40 countries. Not to be left out, American Express has revealed it is exploring how to allow stablecoins to be used on its network. Smaller payment platforms are also engaging with stablecoins - for example, Jack Dorsey (founder of Twitter and reportedly worth over $7billion) has a payment business called TBD, which has tweeted: “We’re partnering with [Circle] to solve some of our biggest money challenges, including decentralized, global on-and-off-ramps between fiat and crypto worlds that can power global use cases from cross-border remittances to self-custody of stablecoins.” Here is a list of other payment platforms offering crypto-related services, but relatively few banks exist which have been prepared to offer on ramp/off ramp crypto services i.e. enable one to buy or sell crypto using a bank account.

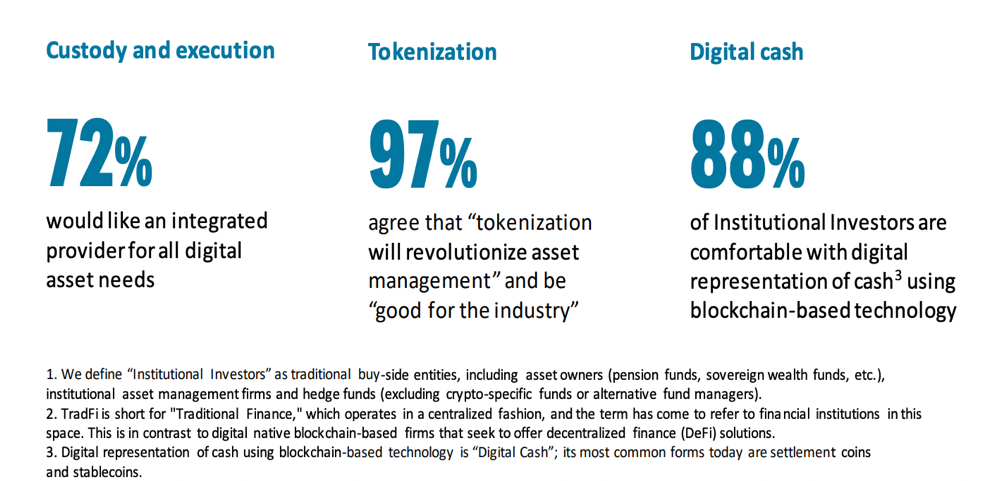

An often-cited question is: “How can I use my crypto?” Well surprisingly, there are literally millions of merchants around the world that accept Visa or Mastercard. Furthermore, via their platforms one can spend crypto using a crypto debit card, such as Crypto.com. Alternatively, there are a host of smaller firms alongside many global companies that accept Bitcoin as a form or payment - 99bitcoins.com lists some of them here. So, for retail investors, it is relatively easy to spend crypto. But you may also question: “Why should I care about crypto?” The fact is, crypto is merely a rounding error and valued at $1trillion - when you compare it to the asset management industry that is worth over $100 trillion, or the real estate sector that Savills cites is worth $326trillion. Well, digital assets have certainly been on the radar for the world’s biggest custodian bank, BNY Mellon, with $43trillion of assets in custody. Furthermore, it has just launched a crypto custody service enabling its clients to hold crypto and have the same protection as if they were holding cash, equities bonds or any other asset. Having surveyed 271 institutions, BNY Mellon has recently issued a report, “Migration to Digital Assets Accelerates” - and the results may surprise some. The research shows that “70% of respondents would increase their digital asset activity if services like custody and execution are available from recognized, trusted institutions. Despite the market downturn, 88% are moving forward with their plans. The study further indicates that almost all institutional investors (91%) are interested in investing in tokenized products”.

Institutions and digital assets

Source: BNYMellon

As BNY Mellon has revealed, whilst the headlines are often about crypto, possibly the real reason behind why (along with many other global financial institutions) are building an infrastructure for digital assets is less about crypto and more about the digitalisation of the financial services sector as this is where the real money is. We have already seen asset managers such as JP Morgan, Abrdn , Kohlberg Kravis Roberts and Franklin Templeton announce they are to digitise funds. Back in 2018, the World Bank issued its first digital debt instrument and now SWIFT has recently made an announcement that it has “successfully shown that central bank digital currencies (CBDCs) and tokenised assets can move seamlessly on existing financial infrastructure”. With a financial infrastructure that encompasses over 11,500 institutions globally, does this means that digital assets could be bought, sold and stored on a Peer2Peer basis i.e., without the need to involve a third party? If this is the case, then, as we see the financial services sector digitally transforming its products and services, many firms will need to revaluate their business models - so, could this be the real agenda?