Written by Jonny Fry

Written by Jonny FryWriters linkdin: https://www.linkedin.com/in/jonnyfry/

Tokens have been used since the 17th century as being “essentially coins that represent a coin of the realm or are ‘good for’ a certain value of product”. People have used also tokens for exchanging goods and services. The concept and use of tokenisation in modern financial markets was developed by a company called TrustCommerce, back in 2001, to store sensitive credit and debit card information.

Credit card firms use tokenisation to replace a client’s primary account number (PAN) with a token, which is essentially a randomly generated set of symbols which are useless to hackers if they were to access the token. A more simplistic way to think of tokenisation is if you go to a casino, you use cash to buy plastic tokens for use in the casino, with the key point being that the tokens themselves have no value outside the casino. According to the publication, fisglobal: “Tokenization reduces risk from data breaches, helps foster trust with customers, minimizes red tape and drives technology behind popular payment services like mobile wallets”. Therefore, it is of no surprise that payment firms have been using tokenisation with the benefits of tokenisation for businesses including the fact that:

-

it reduces risk from data breaches

-

it helps foster trust with your customers

-

it means less red tape for your business

-

it drives payment innovations

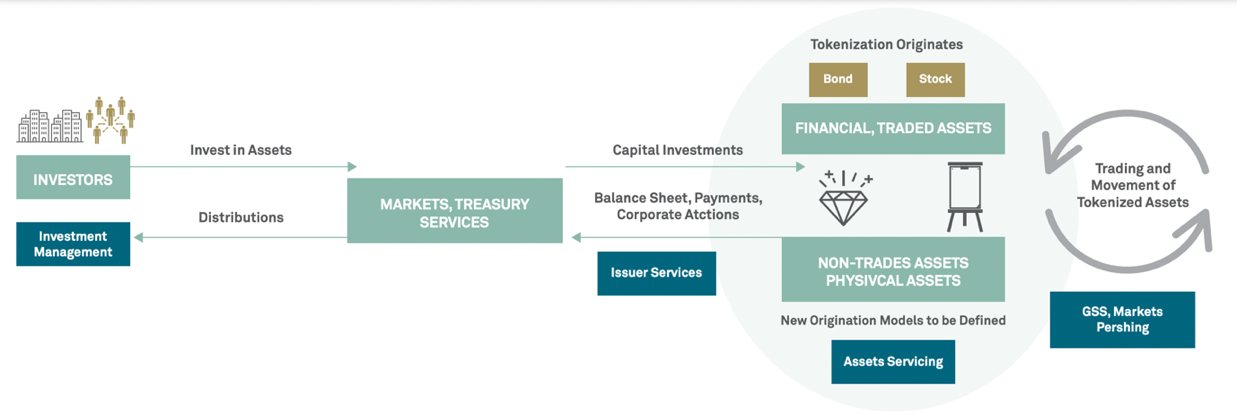

Meanwhile, given the growing understanding and increasing use of blockchain technology, organisations are now using this technology to tokenise not just data, but real assets such as stocks, debt instruments, real estate, commodities, and even cash in the form of central bank digital currencies (CBCDs) and stablecoins pegged to the $ or £ or € etc. Global investments company, BNY Mellon, is one of the global titans when it comes to assets that it looks after for clients, with over $43trillion of funds that it has in custody. It defines tokenisation as: “the process of converting rights - or a unit of asset ownership - into a digital token on a blockchain”, believing also that, “the benefits of tokenization are particularly apparent for assets not currently traded electronically, such as works of art or exotic cars, as well as those needing increased transparency in payment and data flows to improve their liquidity and tradability”.

Tokenisation of assets

Source: BNY Mellon

Listed below is what BNY Mellon believes are the benefits offered by tokenisation :

-

reduced settlement times

-

broader investor base

-

broader geographic reach

-

infrastructure upgrade

-

decreased cost for reconciliation in securities trading

-

regulatory evolution

-

improved asset-liability management

-

increase in available collateral

Whilst tokenisation of equities offers exposure to the gyrations of the underlying stock, e.g., Google, Apple, Mircosoft, etc, tokenised stocks do not offer the legal rights associated with share ownership at the moment - such as voting rights. If you buy a tokenised equity via FTX, you will currently not be able to vote on corporate actions. The same is true for tokenised stocks bought via Binance. However, a feature that could prove helpful for some investors is that FTX is aiming to pay all dividends gross of tax whereby doing away with the need for international investors to be compelled to reclaim tax from various jurisdictions. As well as not being able to vote, holders of tokenised equities also need to be mindful that presently you are unable to buy tokenised shares from one provider e.g., Binance, and sell them on another platform e.g., FTX.

When asked about tokenisation, Clauss Skanning, CEO of Danish firm, DigiShares (specialising in tokenising real world assets), said: “Tokenization is in its essence about digitization, automation, fractionalization, and liquidity. Due to the digitization of assets, we can automate transactions to an unprecedented level and this in turn leads to a massive cost reduction that enables fractionalization. Finally, tokenization enables peer-to-peer trading of assets with no counterparty risk, effectively increasing the value of assets with 10-30% through removal of the illiquidity risk”. Little wonder that both owners of assets and fund managers are looking to tokenise their assets. Also in Europe, 2Tokens, which is partially funded by the EU, is running a series of tokenisation projects to demonstrate the commercially viability of tokenisation in a variety of sectors. 2Tokens has so far been engaged in tokenising bills of landing for the Port of Rotterdam and the Digital Notary, tokenising share registers for notaries in Holland and is also tokenising solar energy parks with a firm called Sunified which has offices in Holland and Australia. Alex Bausch, chairman of 2Tokens, stated recently: “There is a genuine interest and demand for education around tokenisation outside of the financial sector. 2Tokens was founded to be an independent and neutral token advocacy group. Our objective to raise awareness, stimulate relevant discussions, and bring together academics and industrial practitioners to fully explore the real potential of tokenisation and help realize the broader societal benefits.”

By using blockchain technology and tokenising assets, financial institutions are able to become more efficient and improve their risk controls. An example of this is Vanguard, which is using blockchain technology and smart contracts to hedge its exposure to currency volatility. Historically, Vanguard has achieved this by creating swap contracts but now Mark Smith, CEO of fintech company, Symbiont, has said: “The smart contract calculates exactly how much collateral you need based on an initial margin calculation that’s agreed upon amongst the two counterparties. Historically, each side calculates margin on their own, and then they reconcile on an overnight basis or every two days manually to determine if both sides got the right margin variance calculation.” The financial implications of implementing blockchain technology are potentially significant. Roland Berger, has reported that the savings of €4.6billion by 2030 could be generated via tokenisation of share trading. Furthermore, the added transparency and ability to make income payments based on the time a bond, share or a property has been owned as opposed to being paid as income every six months (as is the case for equity dividends), holds much appeal for investors. However, whilst tokenisation offers many opportunities it is yet to be proven on an industrial scale. Clearly there is much education required for traditional regulated firms to understand the technology and compliance implications. This takes time, but already we are seeing assets managers such as Templeton, AllianceBernstein and JP Morgan all announce that they are to tokenise some of their mutual funds - and we are very likely to see other asset managers also follow them in the not-too-distant future. We spoke to Charles Kerrigan, at CMS Law, as one of London’s leading lawyers involved in a variety of tokenisation projects and he said: “ The legal and regulatory issues are now well established and we have experienced service providers supporting projects. Some barriers remain, primarily that large projects take time to work through decisional processes and small projects can get caught up in securities laws if they don’t use exemptions to offer to the public. Our experience is that the market is currently split in two: large (institutional) projects that take the time to work through all the issues to get a prototype stood up; and small (non-institutional) projects that tokenise debt or equity but don’t do a public offer. There is less going on in the middle until the larger projects have proved it out and are public”.

So, it would seem tokenisation offers the potential to transform regulated financial markets as well as impacting on other less liquid assets such as real estate, art, cars etc. But with the tokenisation of cash and mutual funds, could this be the ‘killer’ use case of blockchain technology? Even with this in mind, let us not forget where tokenisation began - with payments with debit and credit cards and by making data transfers safer. The potential to tokenise other data such as loyalty schemes, our healthcare records, and even behaviour, all appear to point to our lives potentially being digitised, monitored and accessible. For many this does not sit comfortably, so one wonders just how far society will want this digitisation and tokenisation of our lives to permeate….