Written by Jonny Fry

Written by Jonny FryWriters linkdin: https://www.linkedin.com/in/jonnyfry/

Bear markets for assets are nothing new and unfortunately neither are the crashes that inevitably follow them. Three of the better-known crashes were: the Dutch Tulipmania (1634-1638); the South Sea Bubble (1720); and the Bull Market of the Roaring Twenties (1924-1929). Of these, arguably the Dutch Tulipmania was a bubble because tulips have never been treated as an investment, whereas equities such as today’s crypto markets have fallen - only to rise again as confidence returns. In more recent times, equity markets have seen asset prices fall sharply on a number of occasions:

-

1972 - 1974: UK 74%

-

1987 Black Monday: DOW Jones 22% in a day

-

2000 - 2002: NASDAQ 75%

-

2007 - 2009: NASDAQ 56.8%

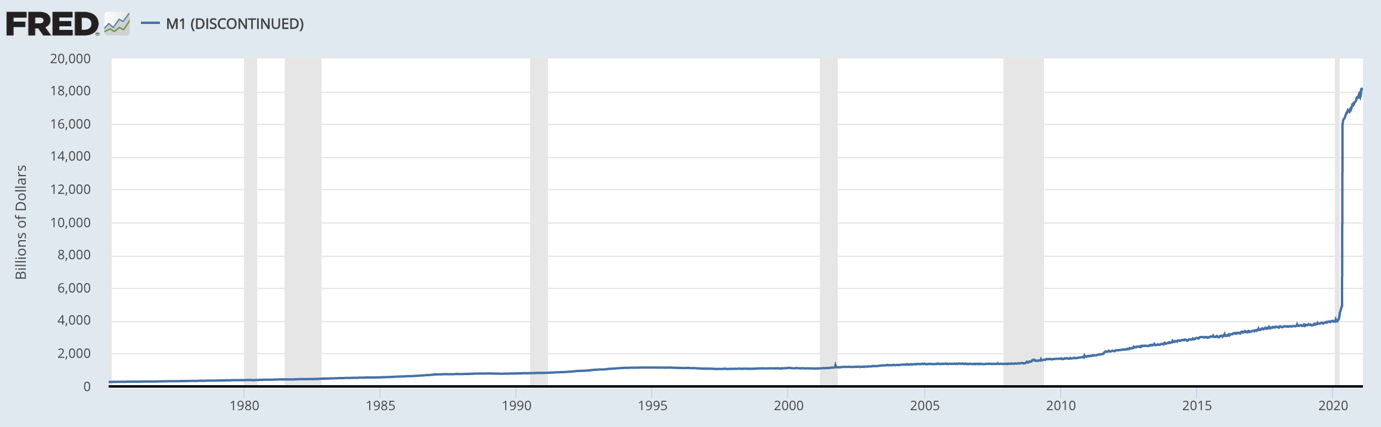

The reasons for falling asset prices often have their roots in what the ex-chairman of the US fed, Alan Greenspan, called “irrational exuberance.” Interestingly, if we look at what Greenspan said in his speech back in December 1996, it may well help to offer some guidance for the current predicament crypto and equity investors now find themselves in - that is, “erratic money, (i.e., wide variations in the quantity of money relative to the demand for money), distorts market price signals and the allocation of resources. Rational economic calculations, especially those affecting investment decisions, become more difficult when the future value of money is uncertain. Inflation and deflation that follow from erratic money undermine both economic and social order”. Well, we have certainly witnessed a lot of money being created, and arguably this has propped up asset prices as interest rates were crushed and companies and individuals went on a credit binge and asset prices inflated. According to the Federal Reserve Bank of St. Louis, 35%+ of all US$ ever printed by the U.S. government was printed in 10 months in 2020.

Source: Fred.StLouis.org

The US was not alone as we saw the world’s central bankers enter into aggressive monetary easing (create cash and buy bonds so reduce interest rates) which had actually started before COVID-19 gripped the world with fear. With all this cash ‘sloshing’ and uber-low interest rates around, it is no surprise that equities, bonds, property and crypto prices increased in value as ‘erratic money’ fuelled an attitude of ‘risk on’ i.e., investors looked for higher risk opportunities which helps to also explain some of the heady valuations of tech stock and cryptocurrencies. The trouble is, is that asset prices are driven also by something incredibly intangible, i.e. sentiment, and once this fickle driver turns it is very hard to regain it in the short term. Having said this, a recent Bank of America survey has found: “Ninety-one percent of 1,013 people the bank surveyed in early June said they expect to buy crypto in the next six months. That is the same percentage as those who actually bought in the past six months.”

Furthermore, one of the challenges cryptocurrencies face is that many of them cannot be assessed using traditional valuations methods. Most of the organisations which have created and issued cryptos generate little income, let alone are profitable, but hold a promise that they will gain mass adoption and one day will be profitable. The crypto market has indeed seen some very large price increases and Bitcoin (still today at over $20,000) has been a staggering investment for those who have held it for 5 years, let alone 10 years. But there are many holders of cryptocurrencies which will be substantially worth less due to their ICO or DeFi or NFT holdings. However, there is an expression - ‘reversion to mean’ - and, given the almost parabolic rise in some crypto prices, it was inevitable that we would see prices fall as reality struck! Nothing ever ‘goes up’ for ever, but a combination of fears over inflation, rising interest rates and the on-going impact of COVID-19 resulting in supply chain challenges, has caused US equities to fall more than 20% from their peak, triggering a bear market. This is on top of the challenges for the so-called stablecoin, Terra, which has fallen in value by over $18billion in a matter of weeks and unnerved investors of volatile high-risk cryptocurrencies.

The market capitalisation of cryptocurrencies ($880 billion compared to its high of over $3trillion) has undoubtably shaken investors. However, cryptocurrencies have helped the financial services sector to embrace digitalisation and challenged the norms. But, in order for cryptocurrencies themselves to thrive and prosper, they need to be able to demonstrate that they, too, offer real financial value to gain greater adoption. The technology (blockchain) that drives cryptocurrencies and the way in which it is able to digitally wrap (i.e., tokenise) real assets such as equities, bonds, mutual funds, real estate, commodities and even fiat currencies in the form of stablecoins and CBDCs, is here to stay. This is due to digital assets being able to i) generate stronger, more effective compliant markets thus treating investors more fairly (a key driver for regulators globally), ii) give greater efficiency and transparency, and iii) remove intermediaries and enable traditional financial markets to be more inclusive. One of the largest banks globally, JP Morgan Chase and Co, recently announced it was to work with the Singapore Central Bank on project ‘Guardian’, with the intention to digitise some of its funds and potentially create $trillions of digital assets. This could “massively increase the assets in the DeFi sector” according to Tyrone Lobban at JP Morgan: "The overall goal is to bring these trillions of dollars of assets into DeFi, so that we can use these new mechanisms for trading, borrowing [and] lending, but with the scale of institutional assets.”

According to Reuters, we are now seeing capital being deployed into infrastructure as investor money searches for, “blockchain-based apps and platforms fuelled by cryptocurrencies that are native to the virtual economies of the metaverse and Web3. VC investment in such projects totalled $10 billion globally in the first quarter of this year, the largest quarterly sum ever and more than double the level seen in the same period a year ago, according to data from Pitchbook”. There is less interest in the ‘jam tomorrow’ type projects that we saw in 2017/18 with ICOs, and more capital is being invested in firms which are promising to be tomorrow’s Facebook, Google, Tencent or Amazon - the digital enablers that other organisations will need to power an ever digitising economy, further and faster. The challenge for cryptos is to keep going, find real use cases that generate revenue and take a few lessons from traditional equities in terms of investor relations. Also, to ensure that token holders are kept up to date in good times and bad, that token holders’ expectations are managed carefully so they know what the company is doing and why (ideally having independent non-executive directors). Transparency, as we have said many times in Digital Bytes, builds confidence and trust which, in turn, will engender positive sentiment and investor support. Yes, some cryptos, like a bubble that pops, will not come back but the crypto market as a whole can restore confidence in investors. Just as we saw following the Dotcom crash, some will bounce back - if only we had a crystal ball to know which ones?