Written by Jonny Fry

Written by Jonny FryWriters linkdin: https://www.linkedin.com/in/jonnyfry/

NFTs symbolise a cultural shift towards a creator-economy and represent your rights to something. An explanation for ‘non-fungible’ can be likened to painting a picture that would not be the same as a picture someone else might paint since the two differ from a rights’ perspective. Yes, you can take a screenshot and copy it, but the digital signature that says “it's mine” cannot be copied. Powerful, because digital ownership is a fundamental concept in this new metaverse-driven world.

‘Atomic swaps’ (a Peer2 Peer transaction) can present a challenge since they make the traditional centralised markets and exchanges redundant because, by using digital assets, we can trade Peer2Peer. An owner of a digital asset (NFT) can bypass traditional exchanges and, in effect, deal direct. For example, you send me a text: “Can I buy your digital painting if I send you 2 Ethereum tokens?”. You transfer the NFT in question (using a blockchain) to my nominated digital wallet whilst, in return, I transfer the 2 Ethereum tokens. All this can take place in a few seconds and, because it is entirely digital, it creates a fingerprint that can be used to prove the authenticity of the transaction having taken place and that it has also been stored on a blockchain to prove who owns what.

Thus, it is easy to see how such digital transfers of rights and digital assets are able to happen 24/7 and makes national boundaries potentially less relevant as buyers and sellers can truly trade globally. However, the lack of centralisation is juxtaposed to the current centralised (almost command and control) structures that we have historically developed in many financial markets and other industries. Typically, regulators and governments prefer to have the ability to hold an entity responsible or accountable in the event that there is a failure or a problem (should one party in a transaction wish to seek redress - for example, compensation). If a transaction has been made via a centralised - typically regulated - marketplace which, in turn, only allows members/regulated entities to trade on it, then a regulator of the marketplace is in theory able to:

-

protect investors

-

maintain confidence in the marketplace.

These two fundamental reasons are why many financial regulators have been established. But if digital assets are to be traded in a decentralised manner this can present real challenges for regulators. Or does it? Afterall, if every transaction creates a digital footprint and is recorded on a blockchain it is possible that regulators could employ smart contracts to monitor decentralised transactions and have access to the monitoring of transactions (which is typically required in the event there is a problem).

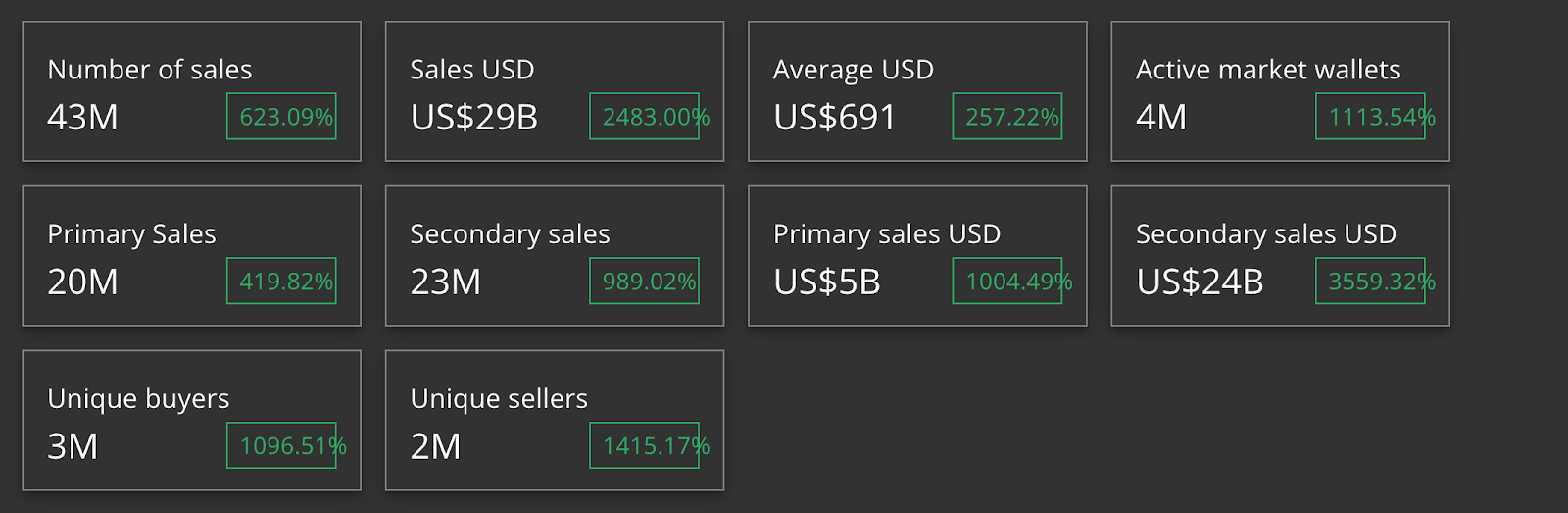

The popularity of NFTs (whilst not as intense as it was in the summer of 2021) is still considerable and is being driven by global brands such as the UK Premier Football League, which has announced it will be offering NFTs to its global fan base. As the table below indicates, the interest grew substantially last year and we are now seeing a very active market in terms of people trading NFTs in the secondary markets.

The growth of the NFT market over the last year

Source: NonFungible.com

A return to self-regulation?

As ever, history is a powerful teacher. Or, as Marie-Antoinette (ex-queen of France) once said: “Nothing is new but what has been forgotten." It was only back in 1986 that we witnessed centuries of self-regulation being swept aside, with the UK creating the Securities and Investment Board (SIB) and the establishment of self-regulating organisations (SROs). As the FT advisor reminds us: “Banks did not need to be licensed until the Banking Act of 1979, insurance companies did not need prior authorisation until the Companies Act 1967”. Therefore, could we see a return to de facto self-regulation where bad actors are identified and then, in effect, banned or excluded? Afterall, such a system has already been employed by organisations such as eBay and Airbnb where users are rated and then made available to all, whereby giving a new prospective trader or provider of accommodation the opportunity to decline conducting business with someone who has a less than savoury track record.

Fractionalisation and the challenges of regulation

Potentially, the use of NFTs and tokenisation creates a whole new way in which physical/tangible assets can be traded. In essence, breaking up the ownership of assets such as equities, real estate, commodities, a picture, etc is possible using NFTs, and this can enable smaller investors to gain exposure to assets that typically they were previously unable to do. Real estate, classic cars, paintings by Michelangelo, etc are all examples, but the challenge is that as soon as you begin to offer any form of collective investment scheme or are seen to be trading in securities (equities and bonds) then the financial regulators’ attention is raised. And such activities mean that regulation is required. Currently, NFTs are typically not regulated or banned in many jurisdictions around the world - even in China where the trading of cryptocurrencies is not allowed but NFTs can be bought and sold. For how long this regulatory position will continue is another question, but then so is how regulators monitor and have oversight of digital assets being traded in the ether as well - unless regulators are given access to the blockchain-powered platforms where these digital assets are being traded. There are proposed regulations in jurisdictions such as Europe’s MiCAR and certainly in the US, the SEC is monitoring the situation to ensure that NFTs are not being used to, in effect, offer securities. Meanwhile, other jurisdictions would appear to be actively embracing NFTs. In the UAE, a law was passed on 22/2/2022 to regulate virtual assets, including NFTs, and Australia has announced that it intends to embrace and regulate digital assets by 2025. The key request by those advising organisations and institutions that are, in particular, looking at being more active in the digital assets sector is proper legal and regulatory guidance so as to avoid being fined/disciplined by regulatory authorities at a later date.

Non-financial assets

NFTs are being actively used in a wide variety of other industries outside of financial services which arguably is where they were first used. On-line games have effectively used NFTs for users to be paid to play, a market segment that is growing rapidly and arguably led by the Vietnamese game developer, Sky Mavis (which created Axie infinity). There now exist Axie scholarships where you are taught how to play and then pay up to 50% of your earnings and, with over 2.5 million active daily players, Axie dominates the NFT pay to play sector. The potential, though, is even greater since the biggest online game is PlayerUnknown’s Battlegrounds (PUBG) with 3,257,248 players. It is thought that one of the ways that Microsoft will be able to recoup some of the $68.7+billion it has paid for the gaming developer, Activission Blizzard, will be by selling NFTs to some of its users. It has already started to poll users as to whether they want NFTs.

In essence, could NFTs be the lotteries of the metaverse? It is predicted that, by 2026, over $433billion will be spent each year on lotteries around the world, yet at least with NFTs you would be given some digital art, even if you lose. Luxury goods manufacturers and global brands are already active in the metaverse with firms such as Bulgari, Cartier, Hublot, Louis Vuitton, and Prada already engaged with NFTs and the metaverse, which is where they are commercialising their endeavours. Global brands such as RayBan, Addidas and Burberry are also all offering NFTs. The global luxury fashion market is expected to reach $352billion by 2027 so the potential market for NFTs is massive, just in the luxury sector let alone high street fashion market.

NFTs are being used to help finance films, are being sold by firms such as Sotheby’s to sell art industry to sell carbon offset credits, being used to transfer patents and to help improve supply chains and logistics. NFTs are also being used to help offer digital identity, undoubtedly a growing need as more people start to use the metaverse and strive to avoid giving their data away for free, such as they have done to the web internet search engines in the past. It is even possible to register your Web3 username on the Ethereum blockchain using an NFT. Ethereum Name Services creates a bespoke digital identity that corresponds to a digital wallet, and these ‘.eth’ domains are represented by an NFT which can be acquired/rented in a similar way that website addresses are. Over 825,000 such addresses have already been generated. It seems that the use of NFTs is limitless, and this presents a real conundrum for regulators. It is understandable why regulators think they need to control those NFTs involved in raising capital (similar to selling an equity), but why do regulators need or want to be involved in museums selling a digital version of a painting, or even your digital identity? NFTs are transforming the way in which we hold and potentially transfer digital assets, both in the physical world and in the growing virtual world of the metaverse. It would seem we have already passed the point of NFTs simply being a fad since without doubt they are set to enter mainstream adoption in a wide variety of industries.