Written by Jonny Fry

Written by Jonny FryWriters linkdin: https://www.linkedin.com/in/jonnyfry/

According to Allied Research: “The global fintech technologies market size was valued at $110.57 billion in 2020, and is projected to reach $698.48 billion by 2030, growing at a CAGR of 20.3% from 2021 to 2030”.

Interestingly, for those people who have cut their teeth in traditional markets or run asset management businesses for over 20 years there is so much that TradFi can teach crypto and DeFi and, interestingly, so much that TradFi can learn from crypto and DeFi. The challenge is, will both types of markets learn from each other? After all, the opportunities for financial markets, investors, regulated firms and regulators are potentially very significant:

-

Crypto trading, liquidity and volumes have the potential to explode;

-

reduced crypto volatility - prices will be harder to manipulate as institutions allocate more capital to cryptocurrencies;

-

TradFi markets will benefit from lower costs;

-

fewer intermediaries;

-

stronger risk and compliance controls;

-

greater transparency;

-

access to a wider audience (potentially the 1.7 billion globally unbanked which the World Bank claims currently exist);

-

trading 24/7;

-

real time analysis of holdings and liability;

-

income payments from equities, bonds and real estate can be calculated and paid based on the length of time these assets are held, as opposed to the current monthly/ six monthly coupon/dividend distribution dates.

The world is becoming ever more digitised and financial markets need to respond, not by electrifying systems and processes but by digitising markets. The ability to automate many of the existing analogue paper-based process and procedures (once data is held in a structured manner) means that smart contracts, big data, machine learning and artificial intelligence can all deployed. This enables much of the compliance monitoring and checking, which is currently largely manual, to be carried out faster and (in many cases) in real time, enabling financial markets to lower their costs and risk profiles, whilst improving the compliance systems and transparency for regulators and management alike. The opportunity to enable regulated firms to create better value products that are more relevant for today’s investors and borrows is tantalisingly close.

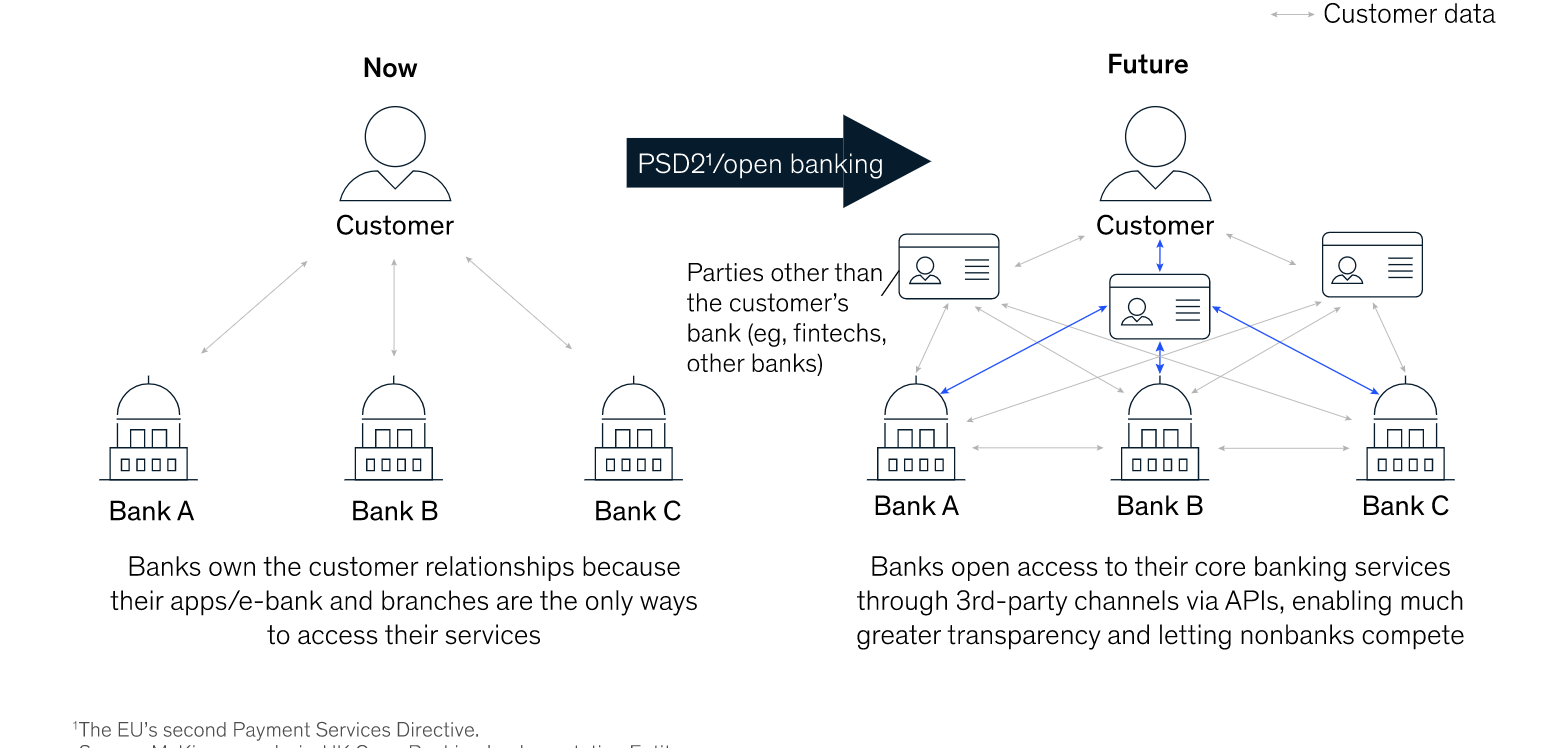

Open banking

Source: McKinsey

Indeed, exciting times ahead for all jurisdictions, but regulators and the regulated organisations need to embrace these new changes as technology while creating challenges also presents real opportunities for these product providers as well as their customers. There is veritable evidence that governments and financial markets are trying to adapt and change, as can be seen by the Open Banking initiative that is being introduced in many jurisdictions. However, so much more can be done. Inevitably, some jurisdictions will be more receptive and those such countries will attract future leaders and FinTech companies and innovators. Thus bringing new products and services but highly paid jobs and therefore much needed tax revenues for debt laden economies, as well as a slew of more relevant digitised offerings.