Written by Jonny Fry

Written by Jonny FryWriters linkdin: https://www.linkedin.com/in/jonnyfry/

Buy and selling property is time consuming, involves large amounts of paperwork and is costly. Indeed, in the UK, the Land Registry advises: “The processing times for updating the register (adding a mortgage or changing ownership) take about 4 to 6 weeks and creating a new register transfer of part or new lease) take about 6 to 9 months”.

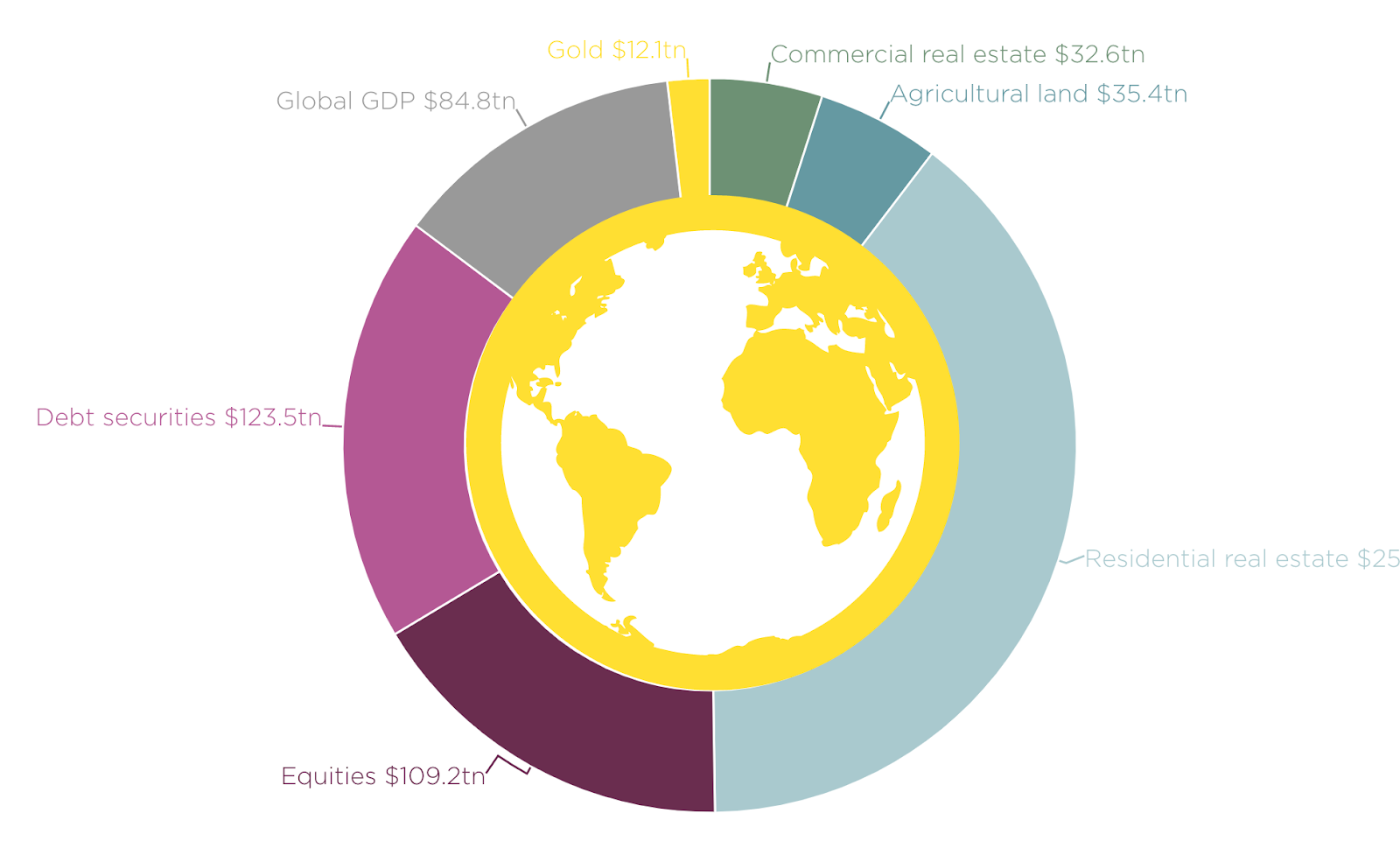

2020 global real estate universe in comparison

Source: Savills Research

If you have ever bought a property, you will be only too aware of the parties involved - lawyers for the buyer, seller, and lender, together with estate agents (realtors in the USA), surveyors, insurance, etc - the list seems to go on. Resultant from this are high fees and the inevitable delays and time to gather and verify the requisite information. Using Blockchain technology to buy and sell property can make this often tortuous process more efficient whereby reducing the time it takes to buy a property and furthermore, seamlessly and accurately recording and enforcing mortgage provisions and conditions in a far more transparent manner.

Potentially, there are three ways that Blockchain technology can help:

-

Digitisation of property ownership interests - there is no reason why one cannot, in effect, create a digital record of the details of a property, not dissimilar to a Non-Fungible Token, (NFT) whether the real estate be a house or a commercial building. A property digital record offers the promise to reduce the time it takes to buy and sell a property and increase the liquidity of real estate which has, historically, been classed as an illiquid asset. Undoubtedly, an extraordinary amount of due diligence is required to identify lien priorities, ownership interests and marketability issues for a particular property before a transaction occurs. However, all these details, as well as other information such as any insurance claims, planning issues, maintenance records etc for the property, could be held then traded and transferred on a blockchain-powered platform. The immutable nature of using blockchains means that the accuracy and trustworthiness of the data eliminates the time needed for extensive due diligence and enables real estate to be immediately transferable.

-

Storage of documents on a blockchain ledger - under the current system, parties are required to request title documents, relying on the fact that the necessary documents are recorded correctly and that there has been no mismanagement between transfers in the interim. By holding all the relevant real estate information in one place and recording this data in a structured manner, it would be possible to track and trace ownership interests of the data and be made available on a permissioned basis for the relevant parties to have access. This would yield a clearer record chain of title for a particular property, thus reducing costs and time to obtain title reports between contract and closing.

-

Enforcing mortgage and loan provisions through smart contracts - mortgage contracts are filled with complex contingencies, covenants and conditions that trigger different default events when they occur throughout the life of the loan. Upon the occurrence of a default event, the typical penalty is an increased interest rate until the breach is cured. Smart contracts can automate this process with greater accuracy (and more quickly) than the largely paper-based analogue systems and process currently used.

As to be expected, there are challenges needing to be addressed before we see the wholesale adoption of using blockchain-powered platforms when buying and selling real estate. The different parties will need to agree to use a new way of carrying out property transactions and, most importantly, each jurisdiction’s land registry would need to be convinced that using blockchain-powered platforms are as safe and reliable as the existing tried and tested systems. Dependant on the type of blockchain (private or public), this raises a variety of challenges around how data is stored. Attention would need to be paid in order to accommodate provisions such as GDPR in Europe, but also the fact that there is no federal data privacy law such as GDPR in the US. There are, however, some national laws in place to regulate the use of data in certain industries in the US, such as the US Privacy Act (1974) which outlines rights and restrictions regarding data held by US government agencies.

The real estate market is immense and any small savings that improve the efficiency of how this market functions will need to be carefully examined. Whilst there are a number of firms looking to offer some form of fractional ownership, the jury is still out as to how popular and effective such offerings are. Blockchain technology certainly offers the promise to fundamentally and radically alter the way property transactions are executed. Some jurisdictions, such as the UK, have now given clarity as to the enforceability of smart contracts.