Written by Jonny Fry

Written by Jonny FryWriters linkdin: https://www.linkedin.com/in/jonnyfry/

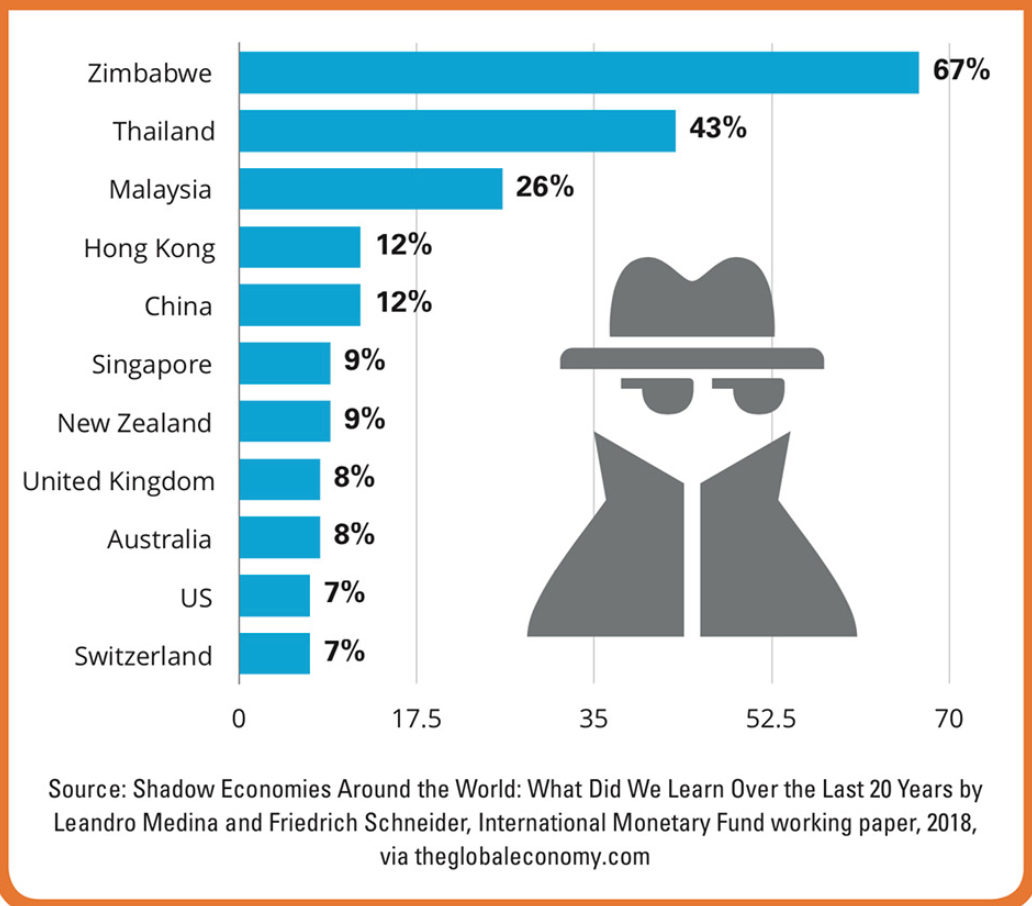

Defined by the International Monetary Fund (IMF) and “also called the underground, informal, or parallel economy - the shadow economy includes not only illegal activities but also unreported income from the production of legal goods and services, either from monetary or barter transactions”. Potentially, every one of you reading this article are (or have at least sometime been) part of the shadow/informal economy, whereby reducing the potential tax due to a nation’s coffers! Who, me? Yes, as you pay a cash tip to someone in a bar or restaurant, pay cash to have your car washed or cash to a plumber or gardener, all of these cash transactions are part of the shadow economy and help explain why it is estimated to be at least $12 trillion of the world’s $82 trillion Gross Domestic Product (GDP) i.e. 15%. Furthermore, according to The Wire, the shadow economy in India is as much as 62%, and worth almost $14 trillion p.a. on its own.

Shadow Economy as a % of the GDP of economy

Source: Acuitymag.com

From research by the World Bank, 31.5% of people over age 15 live without bank accounts globally - that's over 1.7 billion people almost reliant on cash, yet 66% of them have a mobile phone which means they are able to access financial services. One of the ways to tackle the shadow economy is to offer digital currencies and so provide an alternative to cash. Melinda Gates, Co-Chair of the Bill & Melinda Gates Foundation has said “We already know a lot about how to make sure women have equal access to financial services that can change their lives,. When the government deposits social welfare payments or other subsidies directly into women’s digital bank accounts, the impact is amazing. Women gain decision-making power in their homes, and with more financial tools at their disposal they invest in their families’ prosperity and help drive broad economic growth.” Is the Gates foundation or other philanthropic organisations considering the creation of a digital currency to help the unbanked?

Worldcoin is a company that has created a digital currency to be distributed to as many people as possible around the world. Worldcoin is scanning the irises of people’s eyes as a way to prove identity as people receive and then trade Worldcoin.

The potential for digital currencies has not been lost on governments. According to the European Association of Corporate Treasures, over 80% of the Bank of International Settlement members now have various CBDC projects underway. A Dutch fintech-focused think tank, dGen, has predicted in its recent report “CBDCs: Geopolitical Ramifications of a Major Digital Currency” that three to five countries will completely replace their national currency with a CBDC in ten years. The report outlines significant progress in CBDC by jurisdictions such as the Bahamas and also Sweden, where the Swedish Retail and Wholesale Council has forecast that 50% of its high street store members do not plan to accept cash as a method of payment after 2025.

A digital currency could certainly offer governments a new tool with which to control their economies. For example, they could go the extreme (such as the new Chinese CBDC being launched at the Beijing Winter Olympics in 2022) and be able to know who is spending what, where and with whom. Alternatively, CBDC could be used not simply to make payments faster and cheaper but help reach those citizens who are currently unbanked as well as being able to target payments to those citizens in real financial need, without the necessity to pay the banks to act as the distributors.

As for corporations issuing a stablecoin, this potentially enables a far more efficient treasury management with the ability to pay shareholders and debt holders dividends and coupons based on the number of days (even hours) an investor has held the company’s shares or bonds. Stablecoins can offer greater transparency to shareholders, regulators and banks (almost in real time) as regards a corporation’s cash balances. Is it of any surprise then that payment platforms such as Visa, Mastercard, Applepay, Paypal, etc, are now able to transact with digital currencies? As ever, whilst there are sceptics concerned that CBDCs could fuel the shadow economy by enabling payments to bypass existing financial institutions, others such as Metlife Investment Management believe that central banks need CBDCs in order to keep the control of monetary systems from the crypto world, and not allow big techs (such as Facebook’s Diem) to take control.

The banks need to catch up or they will witness firms offering yet more competition, furthermore, undermining the banks with their new financial tools - digital currencies.