Central Bank Digital Currencies (CBDC) is a topic that is regularly asked about by readers. It seems that it is also a topic very much on the agenda for central bankers around the world. The Chinese have already started the rollout of their own CBDC and France, Japan, Sweden, Switzerland, the Bahamas, France, the Philippines and Turkey are all at various phases of testing with a view to launch their own.

Furthermore, CBDCs have very much been on the EU Central Bank’s agenda, and on 14th April it issued a press release updating the public on its findings from a consultation paper about a digital Euro. The three main findings were:

-

citizens and professionals alike value privacy most for a possible future digital euro.

-

preference for a digital euro being integrated into existing banking and payment systems.

-

public consultation to provide valuable input for Eurosystem’s decision in mid-2021 regarding commencing formal investigation for a digital euro.

Interestingly, the consultation paper attracted “8,200 responses - a record participation for an ECB public consultation. A large majority of respondents were private citizens (94%)”. This indicates the interest in a digital Euro/ CBDC and what we believe is inevitable being that it is not if, but when, the EU will follow China’s lead and issue a Euro CDBC. On the very same day, Christine Legarde, head of the EU Central Bank, called for regulation on Bitcoin saying, “the digital currency had been used for money laundering activities in some instances and that any loopholes needed to be closed”, although she did not detail any specific examples on which to base her concerns about how and where crypto currencies had been used.

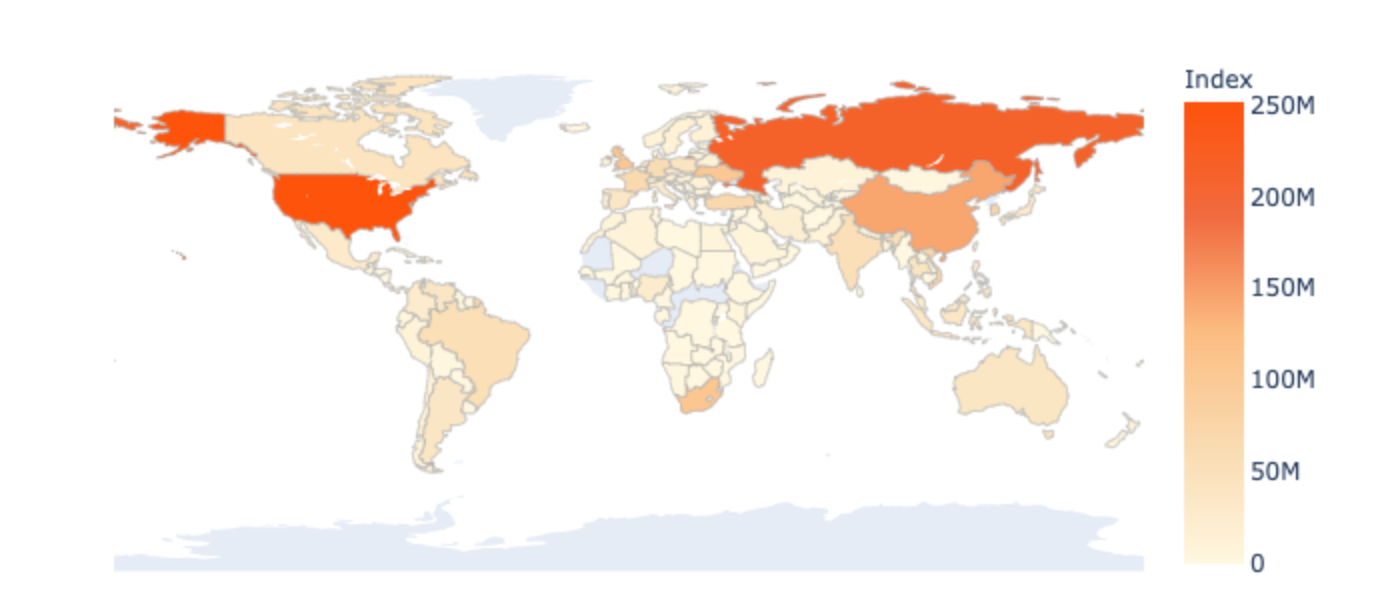

Destination of funds leaving illicit services in 2020

Source: Chainanlysis

However, in a report released earlier this year from Chainanalysis it would seem that the EU is not, itself, a hot spot for nefarious actors using crypto, but Russia and America appear to be where such activity is concentrated. The Chainanlysis report claimed that only 270 digital wallet addresses accounted for over 55% of crypto currency money laundering. The United Nations estimates, $800 billion to $2 trillion is laundered globally each year, accounting for 2%-5% of the global gross domestic product. The UN has not quantified the exact size of the crypto laundering market. However, a report published by MIT (in the US) has claimed criminals laundered US$2.8 billion through crypto exchanges in 2019, compared to US$1 billion in 2018. As of 2019, total Bitcoin spending on the dark web was US$829 million, representing 0.5% of all Bitcoin transactions.

In 2014, Canada became the first country to pass regulation on crypto currencies with respect to anti-money laundering. The first real global response was not until June 2019 when the Financial Action Task Force (FATF) published its guidance for virtual assets and virtual asset service providers (VASP) having stated, “The FATF strengthened its standards to clarify the application of anti-money laundering and counter-terrorist financing requirements on virtual assets and virtual asset service providers. Countries are now required to assess and mitigate their risks associated with virtual asset financial activities and providers; license or register providers and subject them to supervision or monitoring by competent national authorities.” Following on from this, the Monitory Authority of Singapore Payment Services Act (covering firms which were involved in handling crypto currencies) stated that such firms needed to have a license and were required to comply with Anti Money Laundering (AML) regulations. In July 2020, the MAS proposed another set of regulations to control the crypto currency industry in the country.

The European Union (EU) has also introduced legislation designed to tighten controls over the handling of crypto currencies - the Fifth Anti-Money Laundering Directive (AMLD5). This requires companies which have handled or are involved with crypto currencies to register with their local regulator. The EU’s AMLD5 also demands that those companies registering have thorough know-your-customer (KYC) and anti-money laundering AML policies and procedures. This introduction of AML legislation has led to a number of firms offering AML services such as Blockpass, Coinfirm, Jumio, Kompany, ShuftiPro, Tookitaki and Veriff, to name just a few.

CBDCs understandably attract considerable attention as their introduction is bound to impact much of our day to day lives. Their issuance is being spurred on by a relentless drive to digitise our lives and invoke a retirement of paper-based analogue systems and procedures. We continue to witness a decline in the use of cash and electronic transfer of money (which is what we currently have) and instead see them superseded with a digital replacement which offers central banks and governments another tool with which to control their economies - not to mention potentially more insight as to what is being spent, by whom, and where. This enables governments to confront money laundering which is often carried out by drug dealers, traffickers of child labour, prostitution, and illegal arms dealers etc, as well as being able to collect more taxes, more efficiently, as cash-based transactions become less and less.

The question is, does every society wish for its government to have such in-depth insight into the way its citizens spend their money and, indeed, do they trust that their governments will be able to store this information securely and only use this new potential treasure trove of data for the correct purposes?