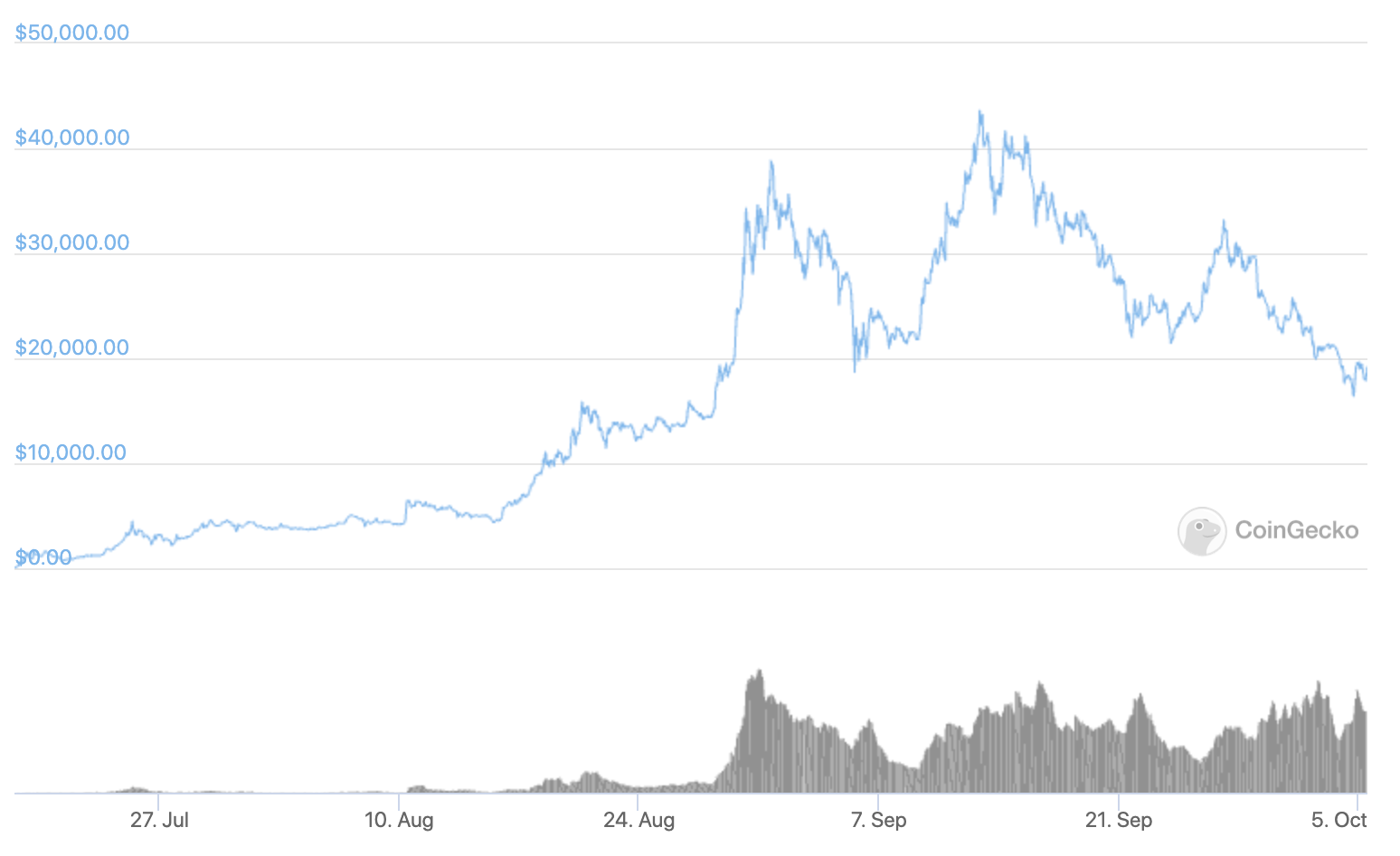

The amount of money that the Decentralised Finance (DeFi) sector has attracted has risen sharply (according to DeFi Pluse.com) from $1.68 billion at the end of June 2020, to over $9 billion in mid-September. This significant level of interest has been fuelled by some of the spectacular returns from tokens such as Yearn Finance (YFI), which increased in value by 6,300% in six weeks as it token’s price rose from $6 to $38,000. Yes, just £1,000 investment at one stage was worth over £6.3million!

A number of firms have been involved in the DeFi sector for years, such as Maker DAO which was established in 2014. However, DeFi really took off this summer. It now offers a range of financial services such as lending, borrowing, insurance, payments, derivatives and even the opportunity to bet on the outcome of elections. This option to profit on the result of an election may offer citizens in some jurisdictions the ability to gamble by buying an asset such as the FTX’s TRUMPWIN or TRUMPLOSE token, even though betting may well be illegal - another question and hurdle DeFi may need to tackle as it gains more widespread adoption. As with anything new and different, education is vital in order to understand the facts before becoming involved. Certainly, if you wish to learn more about DeFi then click here to watch a short video giving a simple to understand explanation of how the YFI tokens operate and are governed.

A term to note which is used in DeFi is ‘yield farming’, being described as the rocket fuel of DeFi since it provides the collateral for many of the DeFi products available. In simplistic terms, it refers to when a holder of a crypto is paid a return/interest, yield (hence the name ‘yield farming) which is far higher that depositing the equivalent amount into a bank account. Unfortunately, given the almost zero interest rates available in banks, DeFi looks almost ‘too good to be true’. This always rings alarm bells as I have heard that expression too many times in over 40 years of studying investments, so please remember caveat emptor- buyer beware as all the glistens is not gold.

Performance of the Yearn Finance (YFI) token

Source: CoinGeko

Andre Crojne, founder of Yearn Finance that created the YFI token which has appreciated so much, has gone out of his way to try and introduce governance and controls, will others have created structures that have proved to be been less Decentralised. An example of a DeFi token that turned out not to be very DeCentralised is Sushiswap, where the chef at Sushiswap was able to take $14million of ETH tokens. The chef clearly had ‘baked-in’ the ability to get control/access of others’ money, but fortunately he could not ‘stomach’ the pangs of guilt and has subsequently handed back the $14million…. Nevertheless, this has to be a salutary lesson for all to check on how DeCentralised the DeFi products and services you are acquiring are, before you buy! Double check the protocols and be sure that someone cannot gain access and walk away with your money….

Furthermore, when studying the DeFi sector there are potentially lessons which Traditional Finance (TradFi) can learn regarding some of the innovation being used in the DeFi sector, as well as the TradFi sector offering lessons for DeFi practitioners:

Jargon free/user friendly language:

In order to gain mass adoption, DeFi needs to have less ‘jargon’ terms such as flash loans, yield farming, staking, liquidity pools, vaults algorithmic market-making APY and even stablecoins (which may not be so stable if they are not 100% backed by $ such as Tether). This type of jargon serves potentially to confuse and, therefore, dissuade new customers to engage.

Education:

Exposure to equity markets is greater now due to the increase in investor education. Just look at any weekend newspaper, or the vast range of investment publications and websites for people to read. However, despite the rise in personal pensions and massive expansion of mutual funds, many citizens are struggling with financial products and services and hence, the need arises for strong regulators to protect investors. TradFi has promoted diversification i.e. promoting funds, as opposed to just buying equities. While companies, such as FTX, have launched the Top 100 Uniswap index, DeFi possibly needs to develop more funds and other ways to diversify the risk of investing in only an individual token. Arguably, DeFi also needs to address the systemic risk of Bitcoin and, to a lesser extent, Ethereum.

Need for KYC/AML:

Money has attracted nefarious actors, and always will. Hence, TradFi insists that before invests are made, clients must undergo comprehensive KYC and AML checks as, in effect, these act as gatekeepers to try and ensure TradFi companies manage ‘clean’ money. Organisations offering DeFi products and services would also be well-advised to start insisting on KYC and AML checks. In doing so it will offer comfort to regulators and governments who have spent years introducing KYC/AML legislation as, rightly or wrongly, they see this a vital plank to help maintain confidence in financial markets. There are allegations that the hackers who stole $150 million from KUCoin have been trying to launder their ill-gotten gains on DeFi exchanges.

Disintermediation:

A term often ‘banded about’ and seen as being good for consumers since, in theory, the less intermediaries involved in a transaction the lower the end price ought to be. DeFi exchanges have manged to do what TradFi exchanges have been barred from - providing market - making services – the setting of prices based on the amounts of assets being bought/sold for customers in order to set the price of an asset. This removes the need for third parties (i.e. traditional market-makers and their fees) by handing control to DeFi exchanges to decide prices.

Trust and confidence:

When dealing with money, trust is paramount since it goes hand-in-hand with confidence. One of the core questions often asked is, “How safe is my money, can someone get access to it?”. The TradFi markets have developed the role for custody i.e. independently third-party firms which physically hold clients’ funds and assets (equities, bonds, etc). Whilst there are a few companies beginning to offer custody for Digital Assets, this is one area which continues to hold back greater engagement into digital assets for many traditional institutions, as legally independent custody providers have to be used. Arguably of equal importance to custody is governance. It should not have been possible for the Sushi Chef to walk off with $14million. The DeFi sector needs to address these challenges in order to allay future potential regulatory scrutiny.

User experience:

If DeFi is to really bring finances to the masses, it needs to find a way to improve the user- experience and not be ‘geeky’. The same way that TradFi previously suffered from being seen as elitist and only for the rich but, by now offering more and more products and services on-line, it is attracting a growing audience who wish to deal via ‘clicks’ and not by talking to a stockbroker or bank manager!

DeFi has certainly experienced a rollercoaster of fortunes in the last couple of months. To survive and thrive it will need to ensure it truly is decentralised in order to avoid the ability for money to be siphoned off/ stolen i.e. it needs to have stronger self-regulation before regulators step in to protect those less-sophisticated investors from another ‘chef cooking the books….’ If it can overcome these challenges, then it could potentially be a massive threat to incumbent TradFi providers. Indeed, there is evidence that some of the DeFi exchanges are already taking the trading volume of some of the larger crypto exchanges, (such as Coinbase and Binanace) which, in turn, have responded by launching their own DeFi offers.