DeFi – Decentralised Finance is described by Forbes as being, “The idea of decentralized finance is that financial institutions can be created that are run by computers, blockchains and rules that anyone can access free of gaining permission or having to show trust or be trusted.” One way to assess the interest in a topic is to look at Google Trends since it records the number of searches that have been carried in each country. By entering ‘DeFi’ and ‘investing’ into Google Trends and selecting the last 30 days you will see that ‘DeFi’ has been searched for on more occasions than ‘investing’ across most of Africa, as well as some of the world’s largest and wealthiest countries such as France, Japan, China and Luxembourg. What is more is, if you only enter ‘DeFi’ into Google, there are 155million results - just try yourself!

Fans of cryptocurrencies often talk about the 1.7 billion unbanked in the world and how cryptos can create a more financially inclusive global society. Cryptocurrencies promise to make money and payments universally accessible to anyone, no matter where they are in the world. DeFi is claimed to be able to go even further than just having the ability to disrupt payments. It is also able to offer a global, accessible alternative to many traditional financial services such as borrowing, derivatives (the largest asset class in the world), insurance, lending, trading, savings and insurance. To access these, all people need is a smartphone and to be able to connect to the world wide web. DeFi services are available to all regardless of who they are, where they were born, or how much money they have. I suspect, though, that KYC/AML checks will be introduced before DeFi becomes a mecca for the inevitable nefarious actors who, like vultures, circle where there is money to be made and prey on those looking for a ‘quick buck’! However, since DeFi is built using Blockchain technology, it offers the transparency and auditability of traditional financial markets but at a fraction of the cost as brokers, dealers (i.e. intermediaries) are replaced

with algorithms and smart contracts. A further advantage is that there is no need to trust to hold your assets in custody or to rely on a third party to settle transactions.

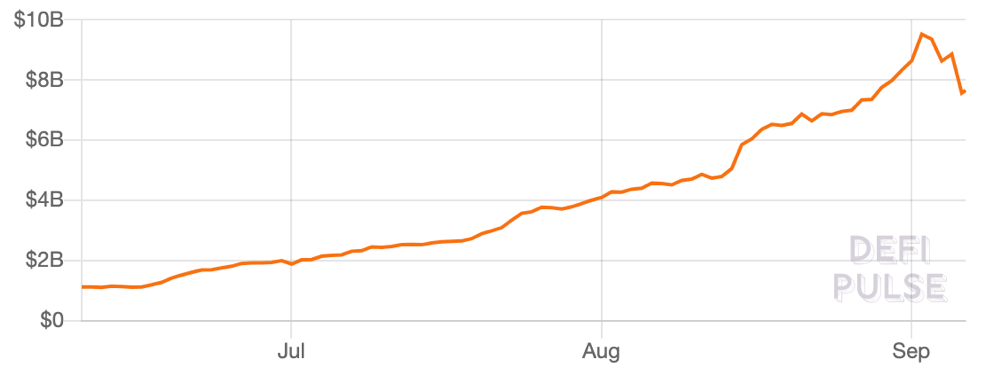

One of the key factors for any market to be able to function and offer scale is liquidity. DeFi liquidity is provided by ‘yield farmers’, i.e. owners of crypto assets who lend cryptos to decentralised anonymous organisations (DAO), The DAOs offer varrious financial services via DeFi applications (DApps) which are run using complex computer codes and executed via smart contracts. The DApps need liquidity and reward owners of cryptos assets by paying them interest/yield i.e. a return, in the form of tokens. Binance states, “Yield farming is a way to make more crypto with your crypto. It involves you lending funds to others through the magic of computer programs called smart contracts. In return for your service you earn fees in the form of crypto.” The amount of capital tied up has grown enormously since the beginning of July 2020 - $1.1 billion rising to, at one stage, over $9.2 billion.

Total value locked in DeFi

Source: DEFI Pulse.com

The way fees are generated for yield farmers is that DeFi exchanges offer the ability to lend, borrow or exchange tokens for a fee. In effect, yield farmers are being paid to provide the liquidity. More important is that the DeFi borrowing, lending and exchanging of tokens is only possible if there are lenders, borrowers and those who wish to exchange assets, meaning there is no reliance on a third party which may, or may not, have the liquidity required. In effect, DeFi has a created an autonomous, computer-based way in which to match buyers with sellers.

But, as ever, DeFi is not a risk-free panacea and there are risks of which to be mindful:

-

crypto volatility - to avoid undue turbulence in the event of the price of cryptos suddenly falling, there is often the necessity to place considerably more than you are able to borrow, i.e. if you wanted to borrow $100 you would need to deposit $200 (200% capitalisation ratio). However, some DeFi exchanges ask for 500% or even 750% capitalisation ratios to try and avoid a sudden fall e.g. flash crashes in the price of a crypto;

-

software bugs - while DeFi is not reliant on third party central clearing houses or financial institutions to settle a transaction it is vulnerable to errors in smart contracts, such as Yam Finance which lost $500,000 to $750,000;

-

systemic risk - as many of the DeFi projects look to exploit the best yields being offered, they generate compound returns by lending and borrowing from each other. So, one major collapse could have serious repercussions in DeFi market;

-

stablecoins – these are often used by yield farmers, and Tether (which has grown to over $13 billion) is one of the more frequently used cryptos despite the fact that it is facing an investigation by the New York Attorney. Were a major stablecoin found not to have sufficient assets then its price could fall, impacting on the value of collateral and, in turn, the DeFi sector;

-

Oracles reliance - the smart contracts which run DeFi protocls rely on Oracles such as ChainLink, UMA, Witnet for information (e.g. the price of different crypto currencies) since, if the price of a crypto that was being held as collatoral were to fall this could result in breaches capitalisation ratios thus leading to the need to close a DeFi exposure. Were these Oracles to be hacked or provide erroneous data, it would undermine the DeFi sector;

-

transaction costs - currently the DeFi sector is very reliant on the Ethereum blockchain and, due to the massive volume of transactions, this has resulted in the cost of processing transactions on Ethereum to sky-rocket from $116 on 17th March 2020, to over $475 on 1st September 2020.

Cryptocurrencies offered the potential to democratise the financial services sector and now DeFi is looking to further disrupt the traditional markets of lending, borrowing insurance and exchanging assets digitally, therefore potentially offering a more efficient and cheaper service. Given the price rises over the last year of tokens such as Loopring (423%), KNC (591%) and Aave (15,309%), to name a few, there is little wonder this asset class is attracting so much attention.