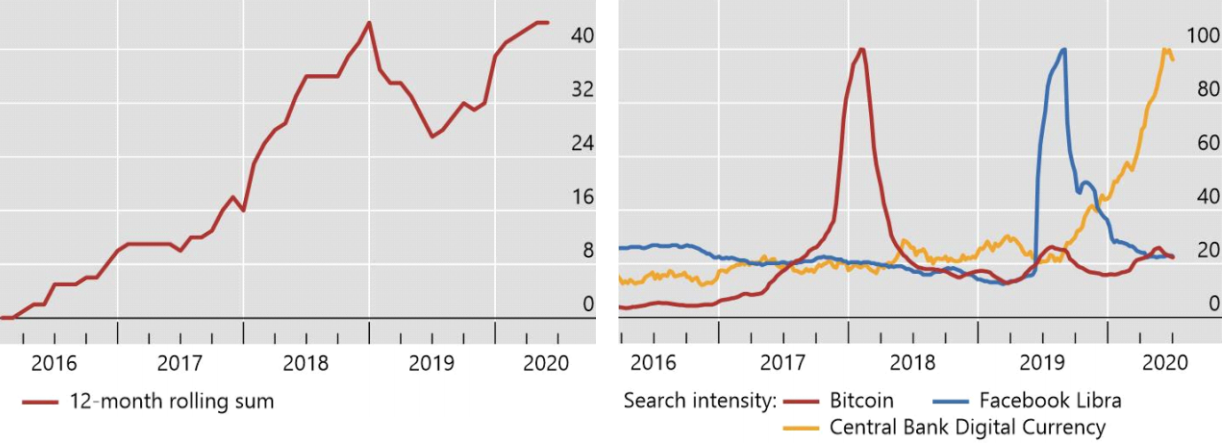

Awareness and interest from academic circles and governments’ central banks studying Central Bank Digital Currencies (CBDC) continues unabated.

Number of speeches and reports on CBDC Google searches

Source: Bank of International Settlement

There have been numerous consultation papers, reports and analyses written by various central banks and global financial institutions such as the International Monetary Fund (IMF), the European Central Bank (ECB) and the Bank of International Settlement (BIS). Indeed, the BIS cite that, as of July 2020, thirty-six central banks have carried out in-depth analysis into the ‘pros and cons’ of issuing a CBDC of their own. The BIS has reviewed summarised various reasons central banks cite for looking to issue a CBDC.

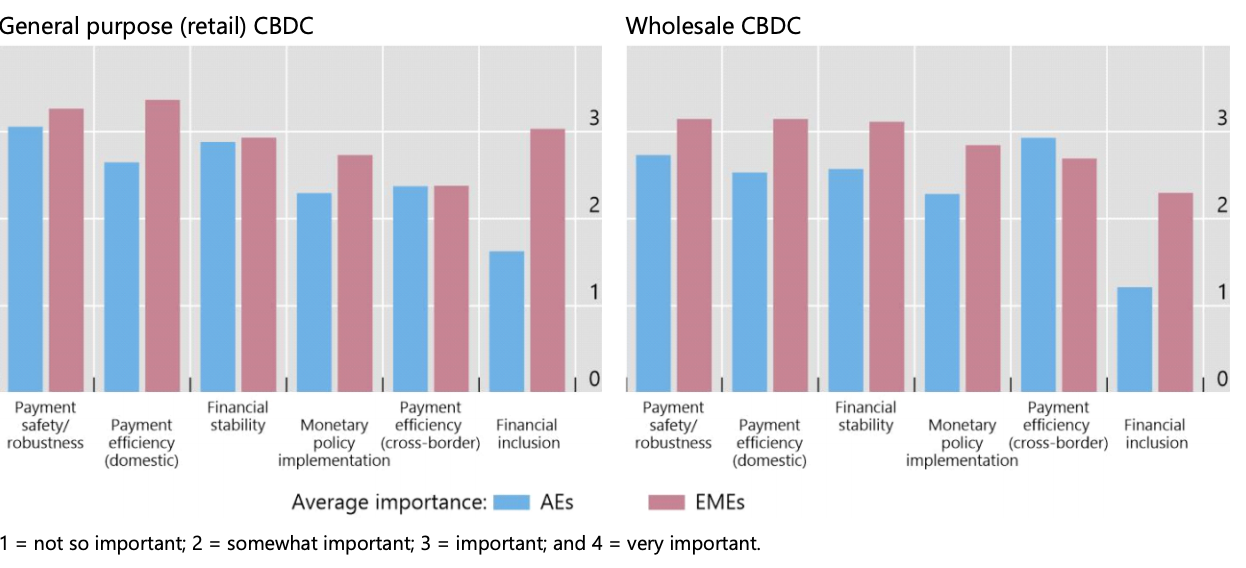

Motivations for issuing a CBDC

Source: CPMI survey of central banks; Boar et al (2020).

The BIS also examined three jurisdictions which have introduced a CBDC:

-

China - reported to be using a mix of centralised and distributed ledger technology (DLT) designed be used alongside physical cash. The majority of Chinese citizens already pay via AliPay or WeChat pay, so these could be the competition not cash that the China’s CBDC needs to overcome. The Chinese have publicly stated their desire to have greater insight to the cash in circulation within their economy and to know ‘who, what where and when’ it is being spent. There it would seem that anonymity of who is spending what is to not be allowed!

-

Sweden - given that many Swedish shops do not accept cash and Swedes use very little cash to pay for transactions, the Swedish Central Bank is using the company R2 Corda to carry out a proof of concept for a Swedish CBDC. The current intention is that the transaction will remain anonymous.

-

Canada - this is interesting, as it has previously been written about in Digital Bytes that the Canadians claim they have no intention of issuing a CBDC. However, extensive trials are being carried out as a contingency in case the citizens wish to adopt one as the use of cash declines, or in response to private cryptos or stablecoins forcing them to respond. The Bank of Canada have also confirmed that it would not have access to digital retail transactions, so anonymity of who and what is being spent would remain

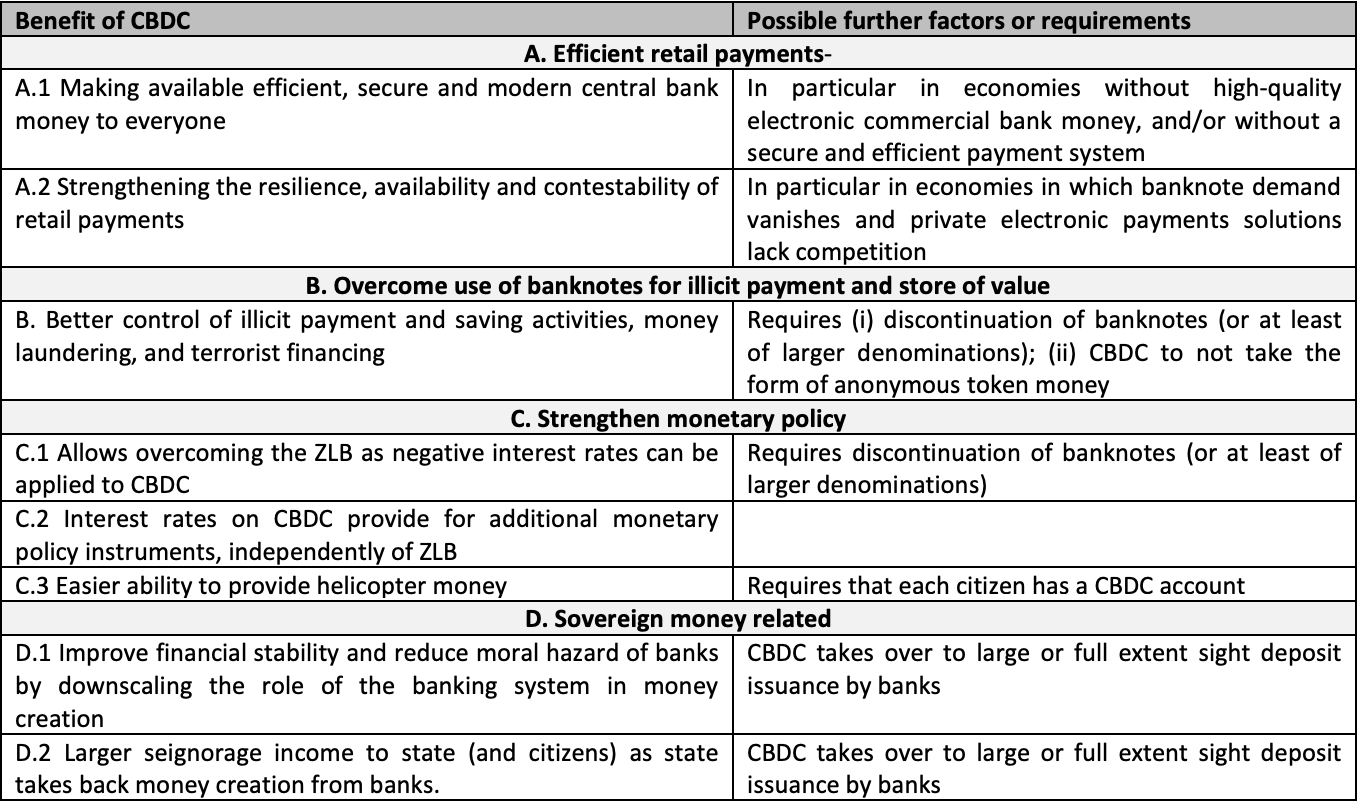

It was proposed in a paper written by the ECB that a CBDC could be seen as a third form of money, the first being overnight deposits lodged with the central bank, the second banknotes. A major constraint for CBDC is that it disintermediates many of the incumbent players so who are likely to resist change. The ECB report also high lights some potential advantages of introducing a CBDC

Overview of benefits that some have associated with CBDC, and related factors or requirements

Source: ECB. Eureop.eu

A working paper from the IMF - “A Survey of Research on Retail Central Bank Digital Currency” - was keen to highlight that given; “most of the major central banks and monetary authorities considering CBDC” this report had been written “not to advocate for retail CBDC issuance, but to take stock of recent research, central bank experiments, and ongoing discussions” This report believes the reason central banks are exploring CBDCs are primarily:

-

to improve financial inclusion;

-

to maintain the central bank’s relevance in the monetary system.

Notwithstanding these reasons, there are other objectives such as the security required and costs of physically handling cash, improving the efficiency of national and global payments, to assist in the battle against nefarious activities, the ability to issue “helicopter cash in a more targeted manner while also being able to introduce negative interest rates as a way to stimulate spending.

However, the IMF report does identify certain risks that central banks may wish to consider before they proceed

CBDC Risk Landscape

Source: IMF

While many central banks wring their hands and contemplate the ‘whys and wherefore’s’ of issuing a CBDC, the People’s Bank of China (PBC) has pressed ahead. China is currently testing its CBDC for small retail transactions in various regions such as Hong Kong, Macau, Shanghai and Beijing with a view to the new Chinese Digital Currency being available for all its citizens in the future.

In the summer of 2019, the launch of Libra raised the idea of Digital Currencies on the agendas of many a bank’s board. Unsurprisingly since then, COVID-19 and the massive decline in the use of cash has given added impetuous. While undoubtably there are many advantages of issuing and using a CBDC, many governments will proceed with caution and possibly only act when they are forced to do so by citizen pressure or competition from other nations digitising their currency first. Given the relentless march of digitisation globally, CBDC could undoubtedly help to make the financial sector more inclusive as well as improving the efficiency of what we earn, borrow and use to make payments.