CurioInvest is looking to offer a range of digital assets backed by classic cars with the intention to actually tokenise 500 cars. Although CurioInvest’s team is based in Zug, Switzerland, it has received approval from Lichtenstein to issue a security token CT1 which will be backed by a 2015 Ferrari F12 TDF supercar. During the first five years, CurioInvest will accept a bid for the Ferrari if the price is more than 20% above the $1.023 million purchase price. If there has been no bid, then the car will be auctioned off and the proceeds paid to the original investors. CurioInvest will be responsible for insuring and storing the car in a highly secure location somewhere in Stuttgart, Germany, and it will earn 20% of any of the profit over the initial purchase price. The tokens that the digitised Ferrari represents will be listed on MERJ, a digital assets exchange which is based in the Seychelles.

CurioInvest is looking to offer a range of digital assets backed by classic cars with the intention to actually tokenise 500 cars. Although CurioInvest’s team is based in Zug, Switzerland, it has received approval from Lichtenstein to issue a security token CT1 which will be backed by a 2015 Ferrari F12 TDF supercar. During the first five years, CurioInvest will accept a bid for the Ferrari if the price is more than 20% above the $1.023 million purchase price. If there has been no bid, then the car will be auctioned off and the proceeds paid to the original investors. CurioInvest will be responsible for insuring and storing the car in a highly secure location somewhere in Stuttgart, Germany, and it will earn 20% of any of the profit over the initial purchase price. The tokens that the digitised Ferrari represents will be listed on MERJ, a digital assets exchange which is based in the Seychelles. A study, with data from 29,002 global auction rooms from 1998 to 2017, was used to ascertain the classic car Sharpe ratio (a measurement that takes into account the volatility of returns i.e. how much the price rises and falls, as well as growth of an asset). Regarding the gross annual Sharpe ratio of classic cars versus those of other asset classes over the sample period it was found that:

-

classic cars, overall, have a higher Sharpe ratio (0.35) than the S&P 500 Index (0.21), the MSCI World Index (0.16) and art (0.07). However, adding dividends would boost Sharpe ratios for the equity indexes to round about 0.30;

-

classic cars have a lower Sharpe ratio than global government bonds (0.40) and gold (0.40);

-

correlations between classic car returns and those of other asset classes are generally low, indicating the diversification benefits within a portfolio of other classes.

The study found that the value of classic cars bought and sold at these 29,000+ auctions was $1.3 billion p.a. Although private sales could boost this figure substantially, the global value of classic cars is estimated to be $130billion.

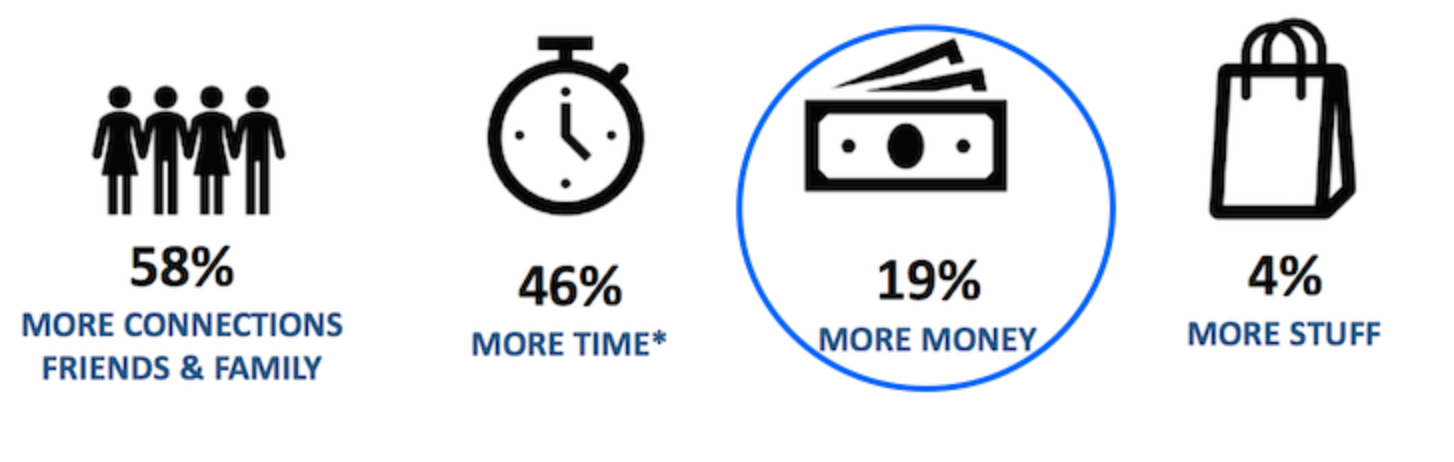

In a survey carried out in the USA by Bank of America it was found that, among its High Net Worth (HNW) clients, there was an average asset allocation to assets of 55% stocks, 21% bonds, 15% cash, 6% alternatives and 4% other. These conclusions imply that the potential demand for alternative and other types of investments, such as digitised exposure to ‘non-traditional’ assets, is very real. So, how long before we see a variety of digital assets giving exposure to assets which have, to date, not been available? Interestingly, when the same cohort of HNW clients were asked, “What would make life better?” - more time and more friends and family were by far the most desired, as opposed to more trinkets i.e. more ‘stuff’!

What would make life better?

Source: Financial Samurai.Com

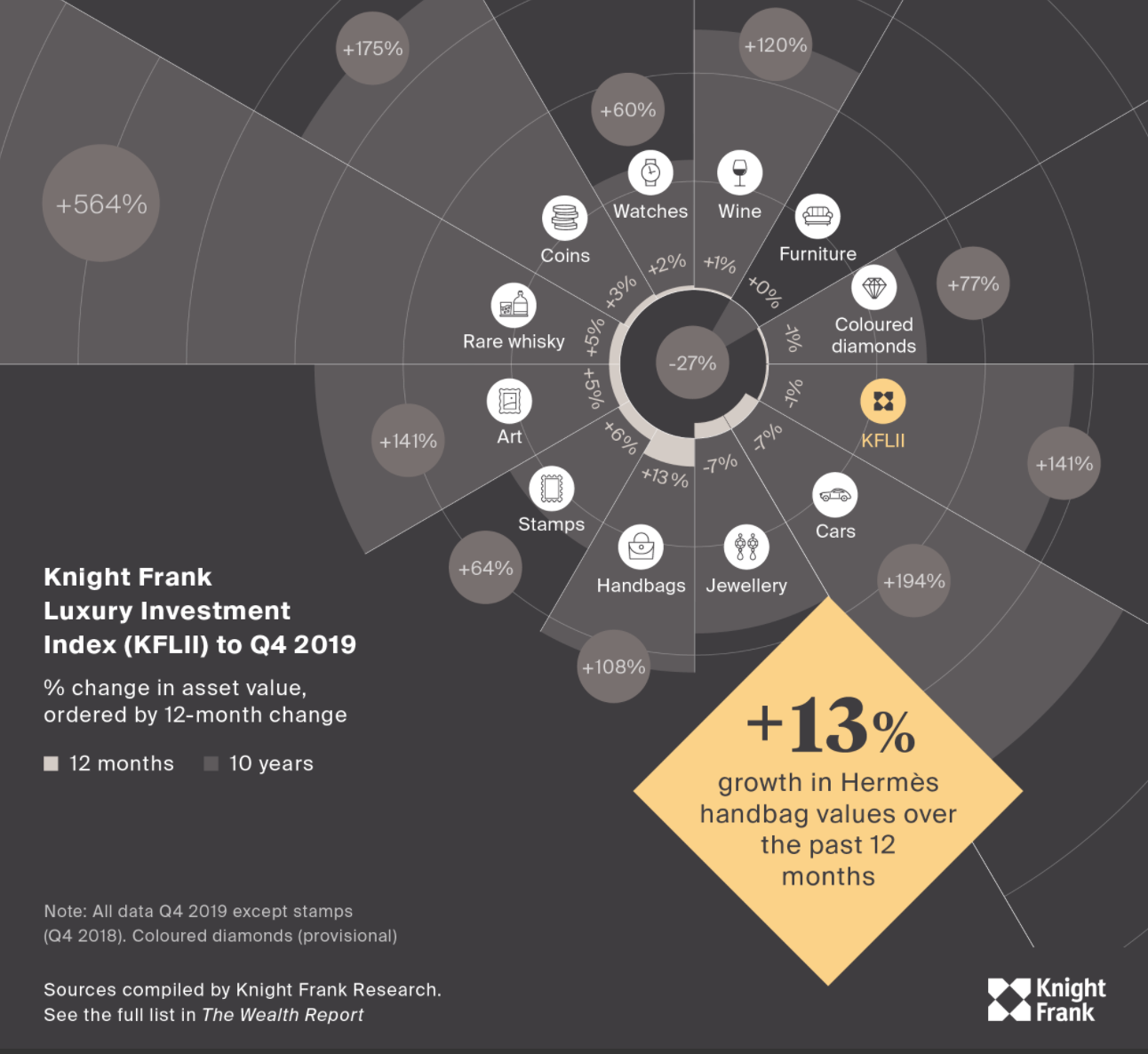

Akin to classic cars, there is a range of other assets which are rare, illiquid and require specialist knowledge to select, store and find in the first place. So, what other assets could be targeted in order to be digitised? Well, Knight Frank (a UK-based estate agent/realtor) has been tracking the performance of luxury goods for a while, and some of the assets which have performed well over the last ten years have been rare whiskey, coins, wine, art and cars.

Knight Frank’s performance of luxury goods

Source Knight Frank.com

There have been digitised/token offerings on most of these but, to be fair, although having raised relatively little capital, such digital assets offers illustrate the flexibility of being able to offer a digitised version of almost any asset class. Digitising these types of assets makes them more affordable for smaller investors, thus bring greater transparency and liquidity. Were we to see a fall in traditional assets (such as equities bonds or property) as a result of the slowdown in economic activity triggered by the Covid-19 pandemic, there could certainly be a propulsion of interest in these alternative assets.