It seems as if every week there is a fresh announcement of how Blockchain technology will impact financial services as another bank, insurance firm or asset manager unveils a different project or investment they have made. Some call it the ‘Internet 2.0’.

It seems as if every week there is a fresh announcement of how Blockchain technology will impact financial services as another bank, insurance firm or asset manager unveils a different project or investment they have made. Some call it the ‘Internet 2.0’.

Without doubt, Blockchain technology offers the financial services sector many advantages. It can help reduce costs, improve transparency, give greater data security and has the ability to create new products and services more relevant and appealing to younger clients (who are typically looking for access to real time information from their mobile phone while on the ‘go’).

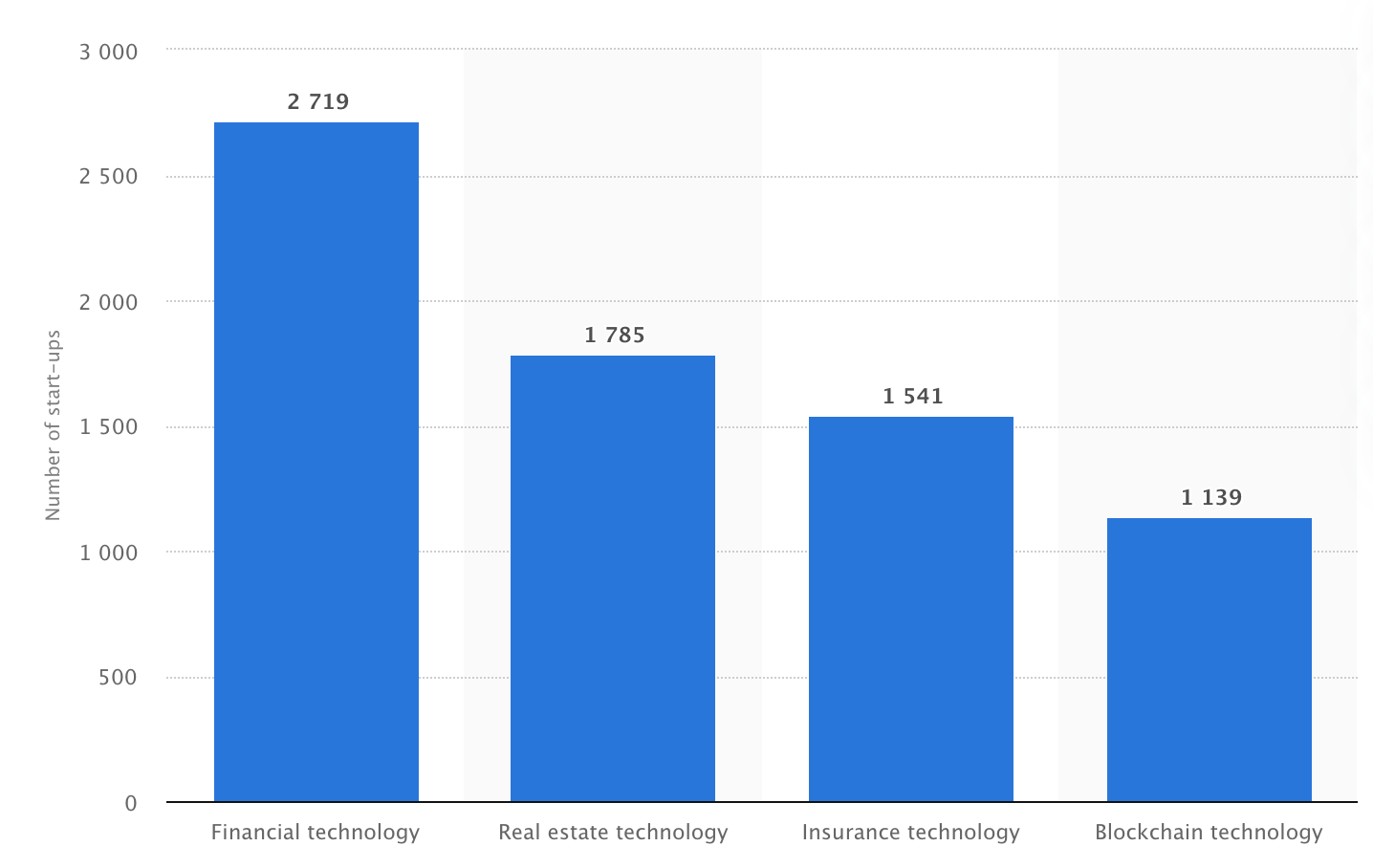

Total number of Fintech, Insurtech and Realtech start-ups worldwide by industry, as of October 2019

Source: Statista.com

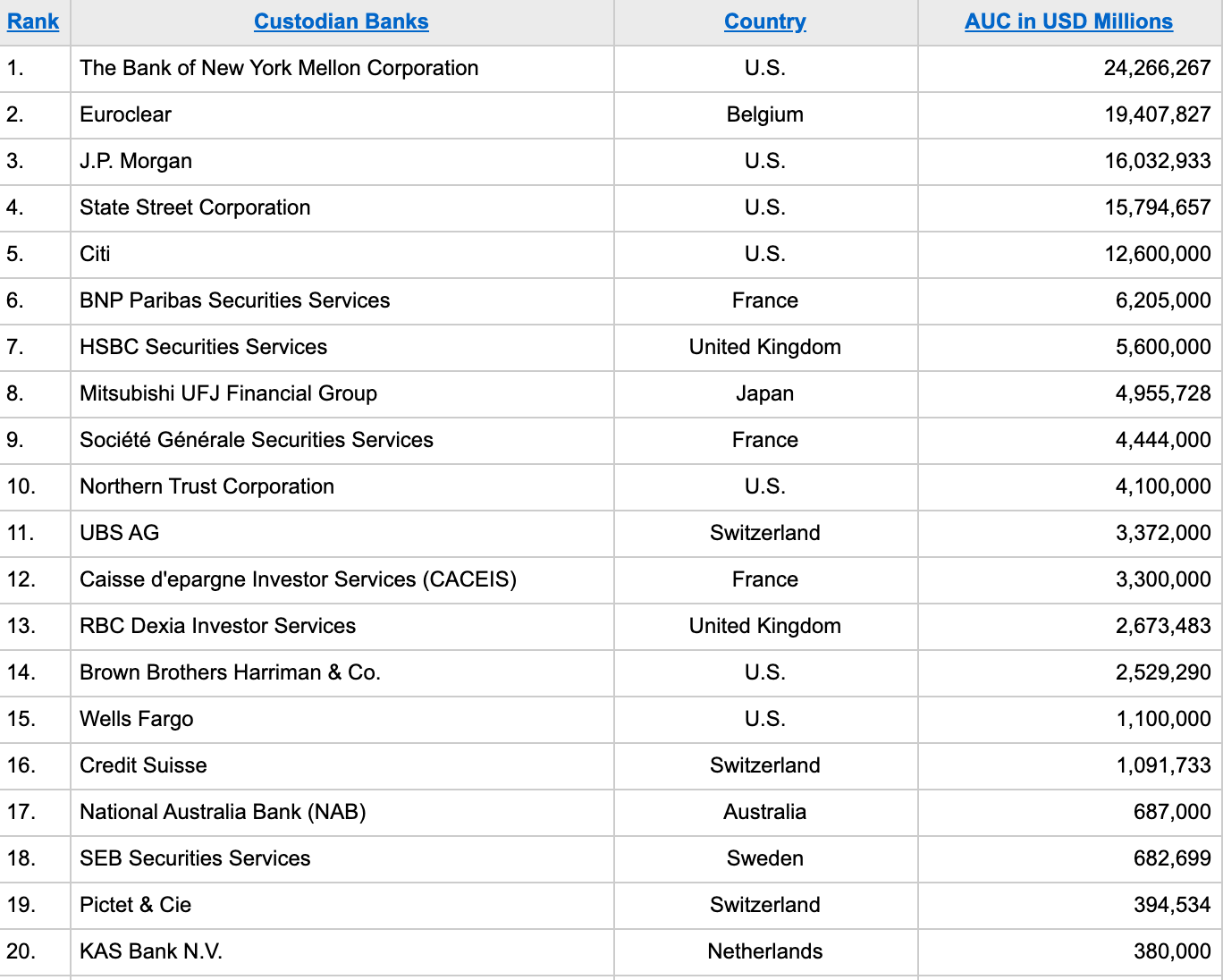

While change needs to be embraced (and there are a host of Fintech firms globally trying to implement this change), the incumbents are unlikely to alter and jump on what some still see as just the latest ‘techy band wagon’. Let us take, for example, custody services offered by banks worldwide - a market that is dominated by only five players. If you are managing assets on behalf of an investor, in most jurisdictions it is a requirement to have the actual assets ‘looked after’, i.e. in the custody of a third party. However, the majority of traditional custody service providers currently do not offer custody of Digital Assets. Arguably this is one of the reasons why it is difficult for fund managers to buy and own Digital Assets, as their existing custody agents are not able to administer them. It also may explain why fund managers often get exposure to Crypto assets (e.g. Bitcoin) via futures traded on established market, such as the Chicago Board Option Exchange (CBOE), as traditional custody service providers are familiar with ‘looking after’ futures contracts but not Cryptos.

A company trying to fill this gap in the market is Custodiex, which has been established by Martin Gymer, an ex-banker who therefore has first-hand experience about what the banks need and currently offer. Gymer recently pronounced, “We know the world is digitising assets like crazy…. Bitcoins and alternative coins, currencies, commodities, documents, property, Intellectual Property, patents, trademarks, customer and business data, paintings, literally everything. At Custodiex we offer a hybrid concrete and cloud solution to look after these digital assets on behave of third parties.”

Custodians by Assets Under Custody

Source: The Asian Banker

The securities industry is certainly one area that is likely to benefit from using Blockchain technology. Enabling trades to be settled faster while providing military grade security helps to explain why possibly JP Morgan has developed Quroum. A Blockchain-powered security would enable dividends to be calculated, based on the number of hours a security had been held, and give real-time access to whom is the beneficial owner of an asset. It would be possible for different types of information to be shared with different parties or different divisions in the same organisation, thus maintaining greater confidentiality and offering enhanced security and privacy (which is impossible using paper-based records requiring masses of documents). At the same time the Blockchain technology would enable regulators to have on-line access to all the data and then, in turn (by using smart contracts),

run exceptional reports to offer real insight to the internal risks and any systemic macro risks in the financial system:

Greater automation holds the promise of better risk control and more time spent on analysing risks, as opposed to checking documents. KPMG claims, “Clients using its Customer Risk Analytics, have reduced the time, effort, and cost of call transcription and analysis by as much as 80 percent”. Furthermore, Blockchain technology offers the potential to impact the payments sector eliminating may of the current intermediaries. It is possible that transactions between consumers could be approved automatically and digital assets could facilitate faster payments at lower fees. This is what Ripple is currently doing with Azimo which, itself, is targeting the Philippine remittance market (valued at over $34 billion p.a.).

Blockchain technology can offer help institutions move closer to real-time transactions between financial institutions and each form will be operating of the same ledger which offer the promise of greater trust as assets can be tracked and trace as they move around the system. HSBC has found that by using Blockchain technology it can substantially reduce the cost of dealing in foreign exchange. Digital Assets, backed by traditional securities such as stocks, bonds, commodities, are obvious evolutions. However, the ability to create new alternative and uncorrelated assets could prove to be really interesting for investors. Such uncorrelated assets could be based on the monetisation of data, Intellectual Property, litigation financing, rental income from Real Estate or an asset backed by a sports star’s future earnings.

Finally, loans and trade finance offer tantalising opportunities. Supposing that the gatekeepers in the loan and credit industry were sidestepped, then the Blockchain could make it more secure to borrow money and provide lower interest rates. Deliotte is of the opinion that Blockchain technology has the ability to reshape the whole trade finance industry. Disruption in the financial services sector will not happen overnight. Blockchain technology, along with machine learning, AI and ‘robo advising’ are all evolving and are steadily making inroads into the financial sectors. In particular, Blockchain technology offers the promise of improving the current financial infrastructure, thus making the latter more efficient. Blockchain technology reduces risks, enables greater automation and, with the use of smart contracts, helps regulated organisations become truly more digital. In turn, this will allow financial service companies to offer new ways for both raising capital and servicing the needs of their clients who, themselves, are demanding real-time products and services - all accessible whilst they are ‘on the go’!!!